CentSai prides itself on writing independent reviews. Check out our rubric to see the objective standards we use.

Highest Possible Total Score:

There are a handful of questions and concerns people dwell on that prevent them from getting involved in the stock market. How do I know who to trust? What if I don’t have enough knowledge and experience? How do I get started?

There are a handful of questions and concerns people dwell on that prevent them from getting involved in the stock market. How do I know who to trust? What if I don’t have enough knowledge and experience? How do I get started?

Although there are known advantages to financial planning, only 33 percent of Americans have a written financial plan, according to Charles Schwab’s recent Modern Wealth Survey. The survey also reveals that 54 percent of those with a plan feel “very confident” about reaching their financial goals.

Many of us have money regrets and trust issues with a market that can feel like it was built exclusively by and for wealthy people. Luckily, platforms like Betterment can help anyone break out of their comfort zone and start investing.

My mom recently boasted about how she began investing and saving for her retirement at my age. I can barely muster up a grocery list, let alone create a financial plan for my future. Although Betterment may be unable to help with my meal prepping, it can provide a time-saving, goal-specific investment platform for people like me who want to get their foot in the door of learning to invest.

About 51 percent of millennials are likely to consider using a robo-advisor compared to 36 percent of Gen Xers and 24 percent of Baby Boomers, according to a recent survey from Vanguard.

I’ve heard one too many times from Baby Boomers that millennials and Generation Z are lazy and entitled. But maybe we simply understand the potential benefits new resources like Betterment have to offer.

The company’s hands-off approach is ideal for beginners, but it also offers features that appeal to experienced investors, with a variety of products and account types.

Betterment uses Modern Portfolio Theory as its magic ingredient to lower risks and stabilize portfolios through the diversification of investments.

The idea is that investing in a variety of asset classes, large capitalization stocks, small stocks, high grade bonds, and so on — in a portfolio optimized through correlations — can reduce your risk for a given level of return.

As the saying goes, the proof is in the pudding, so I thought I’d put Betterment to the test by trying it out for myself.

Ease of Use Score:3

Ease of Use Score:3

For too long, many of us have looked at investing as unattainable due to lack of access and a dire need for financial literacy. The inner workings of investing were coveted, and often seen only as a tool for Wall Street brokers and their wealthy clients.

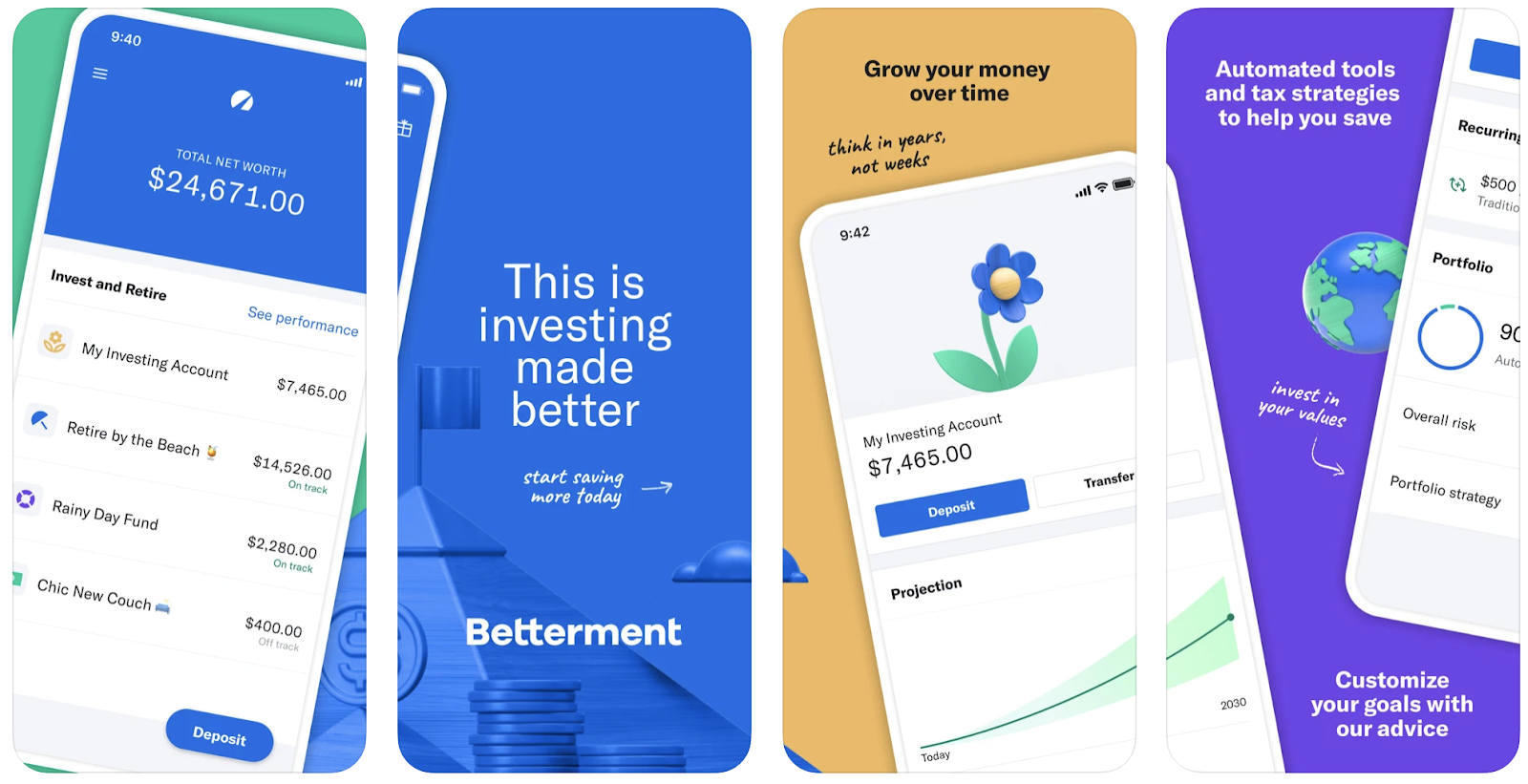

Companies such as Betterment offer features that help people uncover investing possibilities through financial technology. Betterment’s top-rated mobile app gives customers a way to invest from the comfort of their home or the chaos of a rush-hour traffic commute — but no investing while driving, please.

Automatic deposits transfer a set amount from your bank account into your Betterment account so you can regularly invest across different goals such as saving for retirement, college, or a dream home. These transfers can occur weekly, biweekly, or monthly depending on how frequently you wish to invest. Setting it up makes the idea of paying yourself first a cinch.

Betterment also helps you evaluate where to invest, making the process feel hassle free. As a recent college graduate, I am finding my footing. I don’t have the time or energy for that matter, to engulf myself in the nitty-gritty details of global economic trends.

Betterment also helps you evaluate where to invest, making the process feel hassle free. As a recent college graduate, I am finding my footing. I don’t have the time or energy for that matter, to engulf myself in the nitty-gritty details of global economic trends.

This platform takes that weight off your shoulders as its algorithm optimizes every dollar you invest by redistributing across your investments as the market evolves. Betterment’s research and automated strategies — like asset allocation and tax-loss harvesting — adapt how your money is configured, so you don’t have to lose sleep over your financial future.

And for those of you who are interested in being more involved and learning about the ins and outs of investing, the site offers expert-written articles to help inform you on the latest investing news.

Bang for Your Buck Score:4

Bang for Your Buck Score:4

Betterment doesn’t charge a subscription fee, so in order for the company to make money, it charges an annual fee of 0.25 percent for Digital accounts (its more standard option) and 0.4 percent for Premium accounts (portfolios of more than $100,000).

Fees are based on the average daily balance of assets under management, assessed monthly. To put this into perspective, if you have a Digital account with an average daily balance of $10,000 for the year, you would incur an annual fee of $25.

Betterment has no minimum investment amount, no subscription fees, and low management fees of 0.25 to 0.4 percent. Because it is such a large, established company, Betterment is able to keep its fees low.

The platform has no transfer fees or account closing fees, and there is no minimum investment, so you can start investing with $1 as a way to test-drive the system’s operations and efficiency.

Betterment offers a wide array of accounts types including:

- Taxable

- Joint investment

- Traditional Individual Retirement Account (IRA)

- Roth IRA

- Rollover IRA

- SEP IRA

- 401(k)

- Trust Investment Accounts

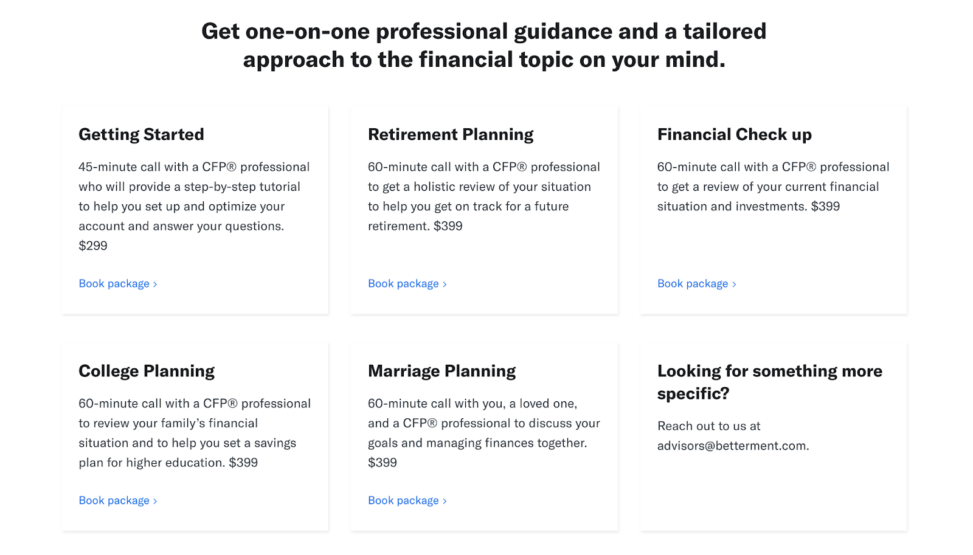

Lastly, having an account with Betterment opens doors to working directly with professional financial coaches. Saving for retirement, paying for college, and marriage planning are just some of the available areas of expertise, with rates starting at $299 for a 45-minute session.

Lastly, having an account with Betterment opens doors to working directly with professional financial coaches. Saving for retirement, paying for college, and marriage planning are just some of the available areas of expertise, with rates starting at $299 for a 45-minute session.

Considering this is only the starting price point, one could argue that Betterment’s financial planning sessions are expensive. For comparison, one of the company’s competitors (Ellevest) offers a 30-minute session for a quarter of the price.

Although the private sessions are a bit pricey, for a rather modest annual fee, Betterment places financial articles, optimized investing algorithms, and personalized portfolios in the hands of its customers.

Customer Service Score:3

Customer Service Score:3

Initially, the sign-up process was a breeze. Betterment requested rather basic information in order to accurately analyze my financial needs, wants, and goals. I was asked for pictures of my driver’s licence and my Social Security card, as well as my birthdate, all rather standard when creating an investment account.

When the platform asked for an additional photo of my face, however, I felt my privacy was invaded.

Although the system was having issues verifying my identity, I was hesitant to hand over these confidential documents, so I decided to hop on a call with a customer service representative. I was blown away by the speed at which I was forwarded to a real person over the phone.

They were informative and kind, and helped me feel at ease about moving forward with the sign-up process by guiding me through Betterment’s privacy policy and the legalities of opening an investment account. It was a rare experience for which I applaud them.

Betterment also provides a nifty feature that allows you to chat with members of its team via text message. All you have to do is enroll, and you can cancel this line of communication at any time.

Reputation

Reputation

Given the numbers, we know that Betterment is popular in the fintech industry. But at the end of the day, reputation counts more than popularity, especially in a market where you are responsible for the future of people’s finances.

Of course, my singular experience is just one of thousands. How does the rest of the world feel about Betterment? Is investing truly any better with this company?

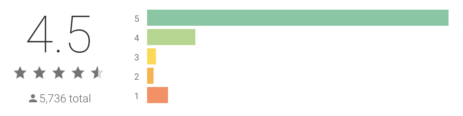

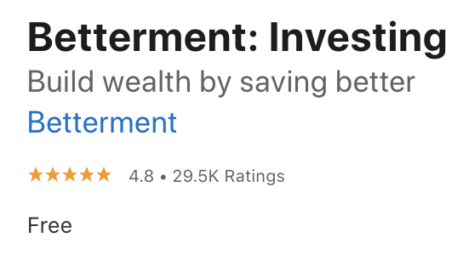

Betterment’s Google Play reviews are nearly spotless, with almost 6,000 reviews averaging out to 4.5 stars. And the company’s App Store reviews are even more impressive, with 29,500 reviews filling out 4.8 of the possible 5 stars.

However, the Better Business Bureau’s (BBB) site tells another story. Betterment has received 11 customer complaints, mostly regarding issues with money transfers and withdrawals, that have left these customers extremely frustrated and downright upset.

However, the Better Business Bureau’s (BBB) site tells another story. Betterment has received 11 customer complaints, mostly regarding issues with money transfers and withdrawals, that have left these customers extremely frustrated and downright upset.

We reached out to Betterment’s press office seeking commentary on its BBB page, but received no response.

It’s imperative to keep in mind that every organization has its flaws, and although these complaints are worrisome, there’s almost always going to be potential risks and uncertainties with companies that provide for hundreds of thousands of unique customers.

The Bottom Line

The Bottom Line

I’m unsure how my mother independently handled her finances at such a young age. I admire her for that. As my mom and many other Baby Boomers would say, my generation may have it easier in a sense because of phenomena like the fintech boom. Regardless of the negative connotation this belief holds, it doesn’t need to be frowned upon.

Betterment is a finely honed robo-advisor that provides a user-friendly customer experience. Its fees are clear and fair, and its goal specific, personalized portfolios speak to the needs of each individual.

Access to money experts, live chats with representatives, and financial journalism are just a few of the perks that come with a Betterment account.

It’s encouraging to witness companies like Betterment propel the level of access and simplicity for beginner investors because it unveils the prospect for greater economic equality.

Although tools like these may only scratch the surface of this global issue, I would like to believe that increased financial resources can slowly bridge the wealth gap and generate opportunities for all.

Past performance is not a predictor of future results. Individual investment results may vary. All investing involves risk of loss.