Whether it’s the white picket fence or the luxury-building perks that drew you in, buying a home for the first time can be just as exciting as it is overwhelming — filled with forms, contracts, and reams of paperwork. Not to mention that it’s a sizable purchase.

These days, the majority of first-time home buyers are millennials, according to the National Association of Realtors (NAR). And since 2002 these first-time purchasers make up half of all home mortgages every year, the Consumer Financial Protection Bureau (CFPB) reports.

And there’s that crucial word: mortgage. The vast majority of home buyers, whether or not they’re first-timers, cannot afford to buy a home outright. And of course, it’s not as simple as taking out a loan — there is so much more to buying a home than just taking out a mortgage to pay for it.

Though almost half of all home buyers look online for properties as their first step, a meager nine percent researched the home buying process online first, according to the same NAR study.

To help, CentSai created this ultimate home buying checklist just for you. Our comprehensive guide will ensure that you’re prepared to venture on your home buying journey.

Step 1: Make a Budget for Your Mortgage

Funnily enough, the first step is not to find your ideal home. Just because the gazebo in a backyard is identical to the one you yearned for as a child, doesn’t mean you can actually afford to own it. First, take a hard look at your finances, and figure out how much home you can afford. The Federal Trade Commission (FTC) has an easy-to-use worksheet for comparing mortgages and other home buying costs.

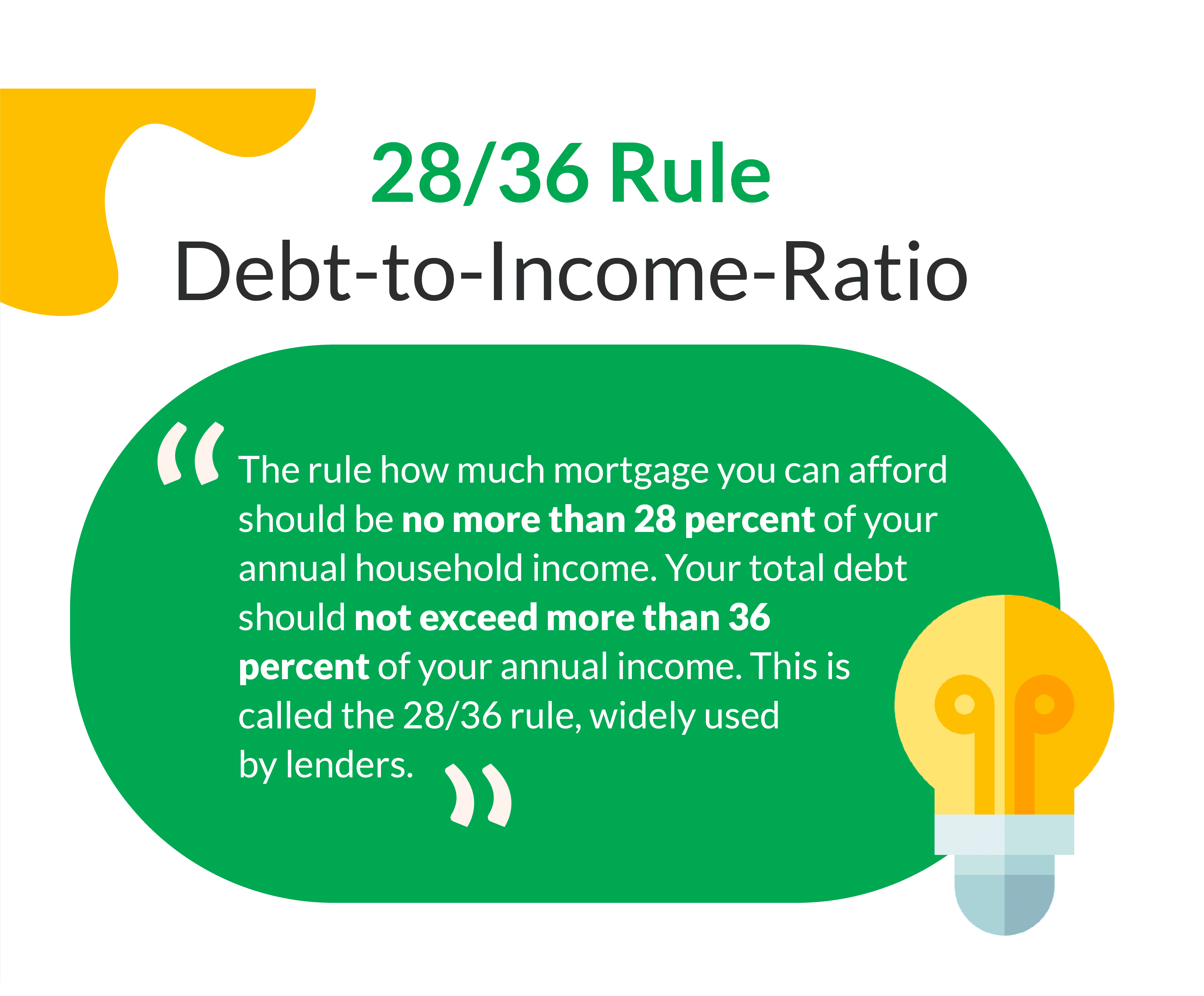

Though there are many resources out there to help you calculate how much of a mortgage is in your (and your spouse’s, if applicable) future, a common benchmark for how much mortgage you can afford comes from an old rule banks used to qualify applicants: the 28/36 rule.

This rule, which establishes the upper limits for approval of conventional loans at many lenders, says that your mortgage obligation (principal, interest, taxes, and insurance) should be no more than 28 percent of your gross income and your total debt, including the new mortgage, shouldn’t exceed 36 percent of your gross income.

Depending on your other obligations, such as the need to save for long-term goals, the actual amount you borrow ideally should be lower than the amount for which you could get approved.

And not getting in over your head is essential, as the higher your monthly mortgage payments, the less money you will have to set aside for retirement or your child’s education, for example.

Remember: Home affordability is not limited to how much of a mortgage you’ll have. There are many costs that you may not have had as a renter.

Consider the maintenance of the home: Will you need a lawn mower, a snow blower or just a shovel, or a landscaping service? Think about your new commute: Is it longer or shorter? Is public transport an option, or will you need to consider getting a vehicle? If you already have a car, will you be driving farther, increasing fuel costs?

Even the geography of your home can have an effect on your bottom line — you may need extra flood insurance in certain areas, for example. Home buying is much more than just principal, interest, taxes, and insurance.

A good start is to consider your current monthly rent or mortgage payment and decide if you can pay that amount or more each month and still have enough money to live comfortably. Calculating your monthly income and expenses will give you the best starting point for the size of a mortgage you should consider.

“While you will want to strive for the best house possible for your money, being able to calculate how much you can spend each month on the mortgage will help you find a price range to consider,” says Ethan Taub, CEO of online lending service Loanry.

“If this is your first time buying a home, the amount of choices can be daunting. Stick to a budget you can afford, and finding a home in your price range will become much easier,” Taub adds.

Step 2: Get a Copy of Your Credit Report

How’s your credit score? Obtain a recent copy of your (and your spouse’s) credit report to ensure it is accurate, up-to-date, and complete. Remember that errors or identity theft can emerge unexpectedly when you pull your credit report. And the good news: The federal Fair Credit Reporting Act requires each of the three big credit reporting agencies to provide you with a free copy of your report each year here (12 months since you last obtained it from that agency).

If you find any errors, the FTC provides instructions and templates of who to contact, when, and how to advocate for yourself to have errors removed.

Bottom line: You want your credit score to be as high as possible to apply for a mortgage. If it’s not, you should consider putting off the home buying process until you can take steps to improve it.

Your credit score directly impacts the interest rate of your mortgage, so generally, a higher credit score can save you thousands of dollars in interest payments over the life of the loan. In general, the lowest credit score that will get you approved for a conventional mortgage is 620, according to FICO.

Step 3: Figure Out How Much of a Down Payment You Need

The next financial hurdle is your down payment. This is a percentage of the cost of the house that you pay up front, and can range from as little as 3 percent up to 20 percent, the CFPB reports.

A larger down payment may leave you with less cash-in-hand right now, but will save you thousands in the future on interest, as a larger down payment means a smaller loan, and the resulting interest cost will be lower.

Similarly to improving your credit, waiting longer to save up for a larger down payment is worth considering. This can be a huge determining factor in your home buying journey, and can help you discern whether now really is the right time to buy.

Remember it can feel like you are missing out on the deal of the century, but don’t let your emotions cloud your judgement, especially on such a mammoth purchase. You are in control, and you pick the ideal time. Don’t feel pressured to make a financial decision you can’t support in the long-term.

Tip: A 20 percent down payment cannot only save you money on interest, but will eliminate your need for private mortgage insurance (PMI) that most lenders require — saving you an additional monthly cost. In Texas, for example, PMI could cost anywhere from 0.5 percent to almost 6 percent of your mortgage principal loan amount, reports the Texas Department of Insurance. This is over the lifetime of your loan, not necessarily yearly.

Step 4: Research Your Mortgage Options

For most people, a mortgage is the biggest loan they will take in their lives. And because the median cost of a house in the United States is over $400,000, according to the Federal Reserve Bank of St. Louis, most people need to borrow money to afford it.

A mortgage is a type of loan typically issued by a bank, credit union, or online lender to purchase a property. The loan is repaid by the borrower, usually (but not always) in monthly installments. Each payment typically consists of the principal (outstanding loan balance) and the interest (the price you pay the lender for borrowing money) of the mortgage. Mortgage loans typically span 15 or 30 years.

Deciding which type of mortgage is right for you is the next step. Mortgages can be broken down into three structures: fixed rate, adjustable rate, and interest only.

Fixed-rate mortgages maintain the same interest rate across the term of the loan — meaning monthly payments are always the same. This mortgage structure works wells or those buying in a relatively low interest rate environment, who plan on staying in their home for a long time.

Though a fixed-rate mortgage typically has a higher interest rate than an adjustable rate one, the advantage is predictability — these rates won’t change on you. The downside is that you are locked in at the same price even if interest rates decline in the market.

Adjustable-rate mortgages (ARMs) have an initial fixed-rate period that usually has lower interest rates and, therefore, lower payments, but they’re not without drawbacks. After this initial period, the interest rate resets, is set for a period of time, then resets again.

With a 5/2 ARM, for example, the interest rate is set for the first five years, then resets every two years. Monthly payments could increase or decrease over time, but there is a cap on each increase, and a total cap, so you can plan to some degree. This option requires caution: You need to be sure your budget can absorb future increases before diving in.

Interest-only mortgages allow the borrower, for a period of time, to make monthly payments of interest only, meaning the principal of the property does not decrease initially.

Typically lower than principal plus interest payments in this period, this type of mortgage is attractive to those who want lower payments in the beginning, or those who don’t anticipate staying in their property for a long period of time, like professional investors, landlords, or others who are looking to exchange building equity for lower payments in the initial years of the mortgage.

Once the interest-only period ends, however, payments are usually higher than a fixed-rate mortgage, for example, and you build less equity in the home as you are only paying towards the interest, not the principal cost. Usually, this mortgage structure is not the best for the first-time home buyer.

There are a multitude of mortgage loan types within each of these structures — for a breakdown of each, as well as the pros and cons, check out our Ultimate Guide to Mortgages here. Do your research with these primary structures in mind to discover what’s best for you.

Step 5: Get Prequalified and Preapproved for Your Mortgage

Now that you have an idea of what you can afford, and which mortgage type best suits you, it’s time to find a lender and get it in writing. As a prospective home buyer, you should shop around and compare lenders, as interest rates and closing costs vary from institution to institution.

Step 1 guided you through budgeting for your mortgage; the next thing to do is make sure you prequalify for the mortgage payment amount you are comfortable with — and that you can afford! Though it’s an optional step, and not a guarantee, prequalification can save you from wasting time looking at properties you can’t afford. Though hopefully, if you budgeted correctly, this shouldn’t be an issue for you.

This is a non-binding step between you and the lender, and is based on the picture you give the lender of your financial situation alone — at this stage, lenders do not verify any of your information. Prequalification should be used only as a rough guideline. This step can be done over the phone or online, and usually costs nothing.

A preapproval, while also optional, makes things easier for real estate agents and lenders. Your credit history, employment history, proof of income and any assets are verified by the lender at this point, unlike with a prequalification. You are preapproved as long as the property meets the qualifications and standards set out by the lender, and there are no changes in your situation.

Once you are preapproved, you will receive a conditional letter for that mortgage amount, which is typically good for 30 to 60 days, according to the CFPB. This increases the real estate agent’s ability to negotiate with the seller on your behalf — if you’re using one — as it strengthens your offer to the seller. Again, preapproval is not a guarantee, just a strong assurance.

“Many times, mortgage companies will provide buyers prequalified mortgage amounts that are actually more than they should be paying for a home,” says Jonathan Faccone, a real estate agent and founder of real estate company Halo Homebuyers.

“It is prudent as a first-time home buyer to fully understand your overall financial picture so you can figure out what you can realistically afford. This means understanding your expenses then adding those that accompany homeownership such as utilities, garbage collection, cable/internet, maintenance, and potential repairs in the near future,” Faccone adds.

Don’t forget: Mortgage lending discrimination is illegal. If you feel you have been exposed to discrimination because of your race, sex, disability, age, or religion, you can file a report with the CFPB, U.S. Department of Housing and Urban Development, or the FTC You can also file complaints with your local Attorney General office, or the lending institution themselves.

Step 6: The House Search

Now that you’ve done your homework to determine how much of a home fits your budget, short- and long-term financial goals, and your lender has given you the provisional go-ahead for the mortgage, it’s time to find the ideal dwelling within your price range (if you haven’t already).

So how do you find this perfect home? If you’re using a real estate agent, specify your price range and any preferences in terms of location, nearby schools, age of home, or crime rates. A good real estate agent can help you narrow down your options — and even bring up factors you may not have considered.

Keep in mind, real estate agents have different levels of experience and styles. Don’t give up if the first one you encounter ends up not being the right fit. As a customer, you should feel at ease and confident that your agent has your best interest at heart. That’s why getting a referral from a trusted source helps.

That said, if you don’t find a match, there are many online resources and databases available to help you see what’s on the market and typical price ranges.

Interestingly, 93 percent of prospective home buyers do most of their shopping online, closely followed by with a real estate agent (87 percent) and through open houses (51 percent), according to NAR.

Search a desired location for open houses and for-sale signs and contact your real-estate agent or the agent selling the home to set up a viewing. Walk around the neighborhoods you are considering, speak to people who live there, and ask them what they like and dislike about their neighborhood.

You’ll likely view many homes, and it can be hard to keep track, so it’s a good idea to keep a notebook where you can jot down standout points about each property.

“I always suggest evening showings as well, when possible, so clients can get a feel of the home in different times of the day,” says Los Angeles–based real estate agent, Jennifer Okhovat.

Tip: Open houses often have a flyer you can take with you, to aid your note-taking. It may also be helpful to ask if you can take photos while you’re there for keeping track. Remember, someone may still live there, so avoid rifling through drawers or closets. Though an open house is an informal event, you do want to be taken seriously, so when speaking to the listing agent so address them accordingly.

Also, pay attention to the agent holding the open house. The more engaged the salesperson, the more likely the engagement will continue and help you through the buying process if you go down that route.

If you’re already working with an agent, let the showing agent know so they don’t continue to solicit you. If you don’t yet have an agent, this could also be a great opportunity to find one. Dress appropriately, wait your turn to view each room if other people are in there, and don’t be afraid to ask questions.

Even though the property will undergo a thorough inspection once you put in an offer, it can be helpful to do a quick survey as you view it to save yourself time down the line. Look for any obvious damage, the state of the flooring and walls — will you need to totally replace or repaint, or will a cleaning-job suffice? — making note of anything you would want to have your inspector to look at for you.

Ask about the age of the electric and plumbing, as replacing parts of either right after closing can be costly.

You may budget for some repairs and maintenance in the short term, but having a realistic idea of what needs to be done will help when making your purchasing decision.

It’s also a good idea to have a list of “must-haves” and “nice-to-haves” in your prospective home, to help you narrow down your choices.

While not impossible, it is unlikely a home on the market will tick every single box — especially if you want multiple flying buttresses and a fountain. So, more than likely, you’ll have to prioritize and compromise on something.

If you have a large family, multiple bedrooms will likely be higher on your priority list, than a dishwasher, a front or backyard, or yes, a fountain. These can be deciding factors between your final home choices once all the must-haves have been satisfied.

“See if the new home fulfills what you may be missing from your current residence. Can you see yourselves spending mornings or evenings in this home?” Okhovat says.

Also, if the color scheme of a kitchen or a bathroom are not to your taste, ask yourself if you can live with it. These rooms tend to be more expensive to remodel, and though you think these “soft” factors won’t bother you — they might once you move in.

Tip: If buying an apartment, “Read the building meeting notes to see what issues it has had previously,” advises Justine Chan, a New York–based licensed real estate agent and founder of women’s home buying site Live With Plum, These can be found on the building’s website or by contacting the property manager. “Make sure to look at the basement — the cleanliness can give you a sense of how well-managed the building is.”

Step 7: Make an Offer on the House

You did it — flying buttresses and all! After doing the math and undergoing research, you’ve found the perfect property. Now it’s time to secure it.

If you’re using a real estate agent, a good practitioner will use their expertise — as well as sales data and knowledge of the market in the area — to help you put forth a reasonable offer to the seller. Remember that these agents work on commission, and you should do due diligence to verify what they tell you, too.

The offer is not always asking price, and could be higher or lower depending on the situation. The agent (or you if you elect not to use one) will draw up a letter or contact the seller to make an official offer on the property. This can also be done over the phone or online, depending on the state.

This is an opportunity to include any contingencies or negotiations you want to make, such as if repairs exceed a certain dollar amount post inspection you have the right to receive your earnest money, or a reduction in associated closing fees. Negotiations can be made on almost anything, but typically include:

- Earnest money

- Inspections

- After-inspection repairs

- Closing costs

The seller can accept, and then you’ve cleared the first hurdle! They could also reject, or counter your offer, to which you can counter, and the cycle goes on until both parties agree, or not. Bear in mind, someone could outbid you at any time, especially if the property is in a popular area at a good price, so locking down your offer early can help ensure you don’t lose out.

That said, it’s a delicate balance. Don’t get in a bidding war out of hubris — know your walkaway price and stick to it. Bidding wars can become fast and furious, and it’s easy to find yourself agreeing to something out of emotion that may not be in your best financial interest.

Once both parties are satisfied, the contract on the property can be drawn up, typically a form with all contingencies and fees, specifying a time to close on the property — all subject to mortgage approval. The contract can be generated by the real estate agent, a broker, a lawyer, or even the seller, depending on your state.

Contingencies are conditions in the agreement of sale that must be met in order for the contract or purchase to go ahead. These conditions serve to protect the buyer during the buying process.

There are multiple contingencies you can insist upon, such as a mortgage contingency: Also known as a financing contingency, this condition says that your offer on the property is contingent upon securing financing within a period of time, usually 30 to 60 days. If unable to secure financing, the buyer can back out of the sale and even get earnest money back.

You can also include contingencies for the home inspection, which will see you get a full report of the condition of the property; an appraisal contingency, which protects you if the sale price of the home exceeds the fair market value of the home; and a title contingency, which gives you the option to back out of the purchase if there are issues with the title on the property.

A final step in making an offer on a home is to pay earnest money. An earnest money deposit (EMD) is monetary proof of how earnest or serious you are about purchasing the property.

It varies from state to state, but earnest money is typically 1 to 5 percent of the mortgage amount paid up front in good faith. This money is then held in escrow — a legal term describing a financial account held by a trusted and neutral third party, in this case on behalf of the buyer and seller. The money you put forward for the property is held in escrow until such a time as the deal has closed.

Earnest money is negotiable with the seller, so don’t dive in headfirst. A trusted real estate agent can help, but exercise due diligence.

While it may seem like a lot of money up front — for example, a 5 percent earnest money deposit on a $400,000 property is $20,000 — you will have to put a down payment on the home regardless, and this earnest money is a great way to get a head start on your down payment.

Be careful of removing any contingencies on the property contract. If you as the buyer agree to remove a mortgage contingency, and your financing doesn’t pan out, you could lose your EMD. In short, do not remove your right to cancel the purchase of the property until you are completely sure you can afford it, get the required financing, and close on the property.

Beware: Sometimes there is a time clause regarding the EMD that requires you to close the sale on the property within a certain period, or you will lose your deposit.

So what happens if you do everything correctly, but your home offer isn’t accepted? Don’t fret. Yes, it can sting, and sometimes dampen the home buying process — especially if it happens more than once. But use this setback as an opportunity to scrutinize your approach to the process. Do you need to adjust your price range? Are you willing to get into a bidding war in the future?

Concentrate on improving your personal finances. Cut your monthly expenditures if possible, thereby saving more and having more money saved for a higher down payment. Also use this time to strengthen your credit score by paying off debt as quickly as possible.

Step 8: Get an Appraisal

An appraisal is required by any lender. An appraiser is an expert who gives an estimate of how much the home is actually worth — the lender uses this to ensure the property value is accurate and not inflated, as they need to know the asset securing the loan has the value it is purported to have, therefore protecting their interest in the property.

If an appraisal comes back lower than the amount you offered, there are a few things you can do.

- Renegotiate the purchase price with the seller

- Increase your down payment

- Negotiate closing costs with the seller

- Dispute the appraisal

- Cancel the sale

The lender won’t pay more than the home valuation, and neither should you. If the seller ignores the appraisal and refuses to budge on price, it may be wise to cut your losses if you can’t negotiate a fair agreement.

If you have signed a sales contract, once you have the aforementioned cancel contingency in place, you retain your right to cancel the sale at this point. Your sales contract should state what happens to your EMD should you default on the sale. If you waived the cancel contingency for example, you may lose your EMD, as well as all application and attorney fees.

Remember: Since the EMD is held in escrow, you are not dependent on the seller to return it to you. You should contact the escrow holder (he bank, credit union, broker, or lawyer) who is required to return it to you usually within 20 days — though this can vary state to state — providing you were within the contingency period to cancel on the sale.

If you believe your EMD is not being returned in a timely fashion, the first step is to write to the escrow holder i. If there is a dispute with the seller, contact them in writing; if that does not resolve the issue, small claims court can be used as a last resort.

This is why ensuring you remain protected with contingencies in the contract is important. Things can and do take unexpected turns all the time, and you want to be sure your hard-earned money is protected.

Step 9: Get a Home Inspection

A home inspection, also required by any lender, is a physical run-through of the property to look for any damages to the home. This can range from peeling paint in the stairwell to costly structural issues.

The inspector plays a critical role in what is likely the most expensive single purchase you make. As such, you should start researching home inspectors early on, perhaps get a referral from a family or friend. If not, try online communities such as NextDoor or Yelp, or trusted agencies like The American Society of Home Inspectors or The International Association of Certified Home Inspectors. Though your real estate agent may want to recommend a home inspector for you, you should do your own research too.

This is, again, an opportunity to negotiate so that any major defects are fixed before you close on the sale — or negotiate to deduct the cost of repairing the defects from the overall selling price — once you and the seller get a neutral third-party estimate of the associated repair costs. It’s your right to ensure fairness and transparency in all parts of the process.

The cost of a home inspection has a typical range of $279 to $399, according to Home Advisor, but this depends on your location. A home inspection in Connecticut averages $480, whereas in Michigan it’s only $290.

Step 10: Close On Your Home

By now, you will have completed the mortgage application, which includes providing the lender with all details of your financial life, and signing all the necessary and supporting documentation, such as the promissory note that states your intent to repay the mortgage. Once approved, you should receive a Closing Disclosure with all closing fees and conditions laid out, from your mortgage lender, at least three days before closing.

At this point, you are required to present the remainder of the down payment and any other closing costs, such as PMI if needed. There may also be the opportunity to pay discount points to offset the overall cost of the mortgage, whereby one point equals 1 percent of the amount financed through the mortgage. This will lower your lifetime interest rate.

On closing day, you will typically meet with the lender in person to sign the closing documents, usually at the escrow holder’s offices. Though this varies from state to state, the seller is not often required to be there, but can be, along with the escrow holder, attorney, and real estate agent, if applicable.

You’ll pay any remaining costs, usually in the form of a cashier’s check. If the seller is present, they will sign the documents that transfer ownership of the property to you. If they are not present, they will have signed these documents in advance.

This is an opportunity to carefully review the documents you are signing. If something doesn’t match up, don’t sign until everyone is one the same page.

Note: If using an online lender, there may be an option to close online — however this often still does not eliminate the need for an in-person signing. Each state has its own laws surrounding this. Currently, most states 28 states allow a complete remote online notarization, and the federal government is attempting to pass legislation mandating that all states allow it.

For a more in-depth look into the process, check out our guide: Everything You Need to Know About Home Closing Costs.

Final Thoughts

Congratulations, you’re now a homeowner! Well, if you followed all of the above steps to a T, you’re on your way.

Though it can seem overwhelming at first, the home buying process does not have to be a stick-your-head-in-the-sand-and-wait-for-it-all-to-blow-over ordeal. Once they have gone through it, almost two-thirds of home buyers are “very satisfied” with the overall process, according to NAR.

It takes most people a matter of 10 weeks to complete their search looking at a median of nine homes, the same NAR study reports. Yes, that means in just over two months, with the right research and preparation, you could be a homeowner. Take control of the process and make sure your credit is in shape, you save enough for a down payment, and you realistically calculate the exact amount of home that’s affordable for you.

Now go get your keys!