I’d been sick with the flu for nearly a week already when I woke up one morning with a distinct twinge in my right lung. I knew it wasn’t good sign. So I decided to finally go to the doctor.

Normally, I’d be panicking. I don’t have the best health insurance through my work, and I knew that the trip would be expensive. I even needed to get chest X-rays. The doctor prescribed me a whole medicine chest full of pills and syrups. If I had waited to go see the doctor, though, my illness would have taken a turn for the worse.

Looking to Reach Your Financial Goals? Start Saving Today >>

Instead, as I left the doctor’s office, I breathed a sigh of relief (albeit a bit haggardly). Why? Several months ago, I started saving up $100 a month to cover unexpected healthcare expenses. I had $500 sitting in my savings account earmarked for just this case. I was prepared.

Emergency Funds Alone Weren’t Enough

After living paycheck-to-paycheck for 10 years, though, I wanted a bit more protection. I knew that I could count on some “unexpected” expenses to crop up. I knew that I would probably get sick and need to see a doctor at some point. It was inevitable that I would need to pay for truck repairs; and that, every so often, a bill for auto and renter’s insurance would show up.

I thought about all the ways I could prepare myself for these expenses. Eventually I came up with the idea of setting up mini savings “accounts” for each of them. I’ve been told that I am like a general readying for a battle. I look for the possible breaches that can occur and try to fortify each area with my “forces” – a dedicated fund.

Build an Emergency Savings Fund With a Money Market Account — Get Started >>

Different Savings Strategies for Different Goals

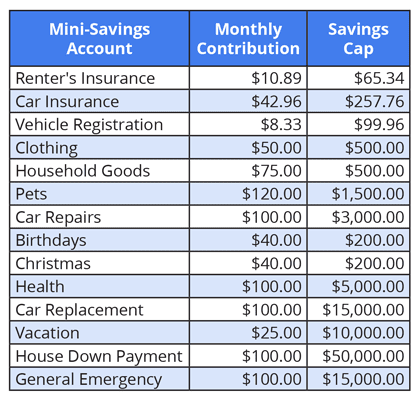

We manage each of our mini savings accounts differently. Each account gets a monthly contribution until we reach a certain savings cap. At this point we stop putting money in that account. All of our money goes into one single high-interest online savings account, but we earmark the money to different goals.

We use budgeting software to keep track of this. But you could just as easily do it with a spreadsheet, or even with pencil and paper. Here are all of our mini savings accounts, how much we contribute to them each month, and the savings cap for each account:

For some of our mini savings accounts, we set the cap at an arbitrary point that we decide is enough for that goal. For example, we save until we reach $200 each in our birthday and Christmas accounts. We can usually reach these goals pretty easily, and it feels great to have a full amount saved for these small things.

Reach Your Savings Goals Quicker With a Savings Builder Account — Start Earning Today >>

For others, we figure out what our largest expense might be, and we save until we reach that point. For example, we’re saving until we reach the out-of-pocket maximum for our health insurance ($5,000), or what we think the largest repair expense would be for our truck ($3,000). That way, when the four-wheel drive went out on our truck last fall, we already had $900 saved to cover the cost of the repair!

Infrequent Bills Don’t Surprise Me Anymore

I never could keep track of insurance bills. So I always was surprised and annoyed each time they showed up in the mail. Now I put them on my calendar. I set aside a certain amount of money each month so that I’m prepared when the bill comes due. This month, our semi-annual auto insurance bill – for $257.76 – came in the mail. Because I’ve been saving up $42.96 per month for the past six months, I already have all the money I need in my account so that I can pay this bill.

What’s in Store for the Future?

Now that I’ve streamlined my system so that I’m not caught off guard by unexpected or infrequent expenses, I’m excited about the future. I am actually able to save more money now than ever before, and it feels great.

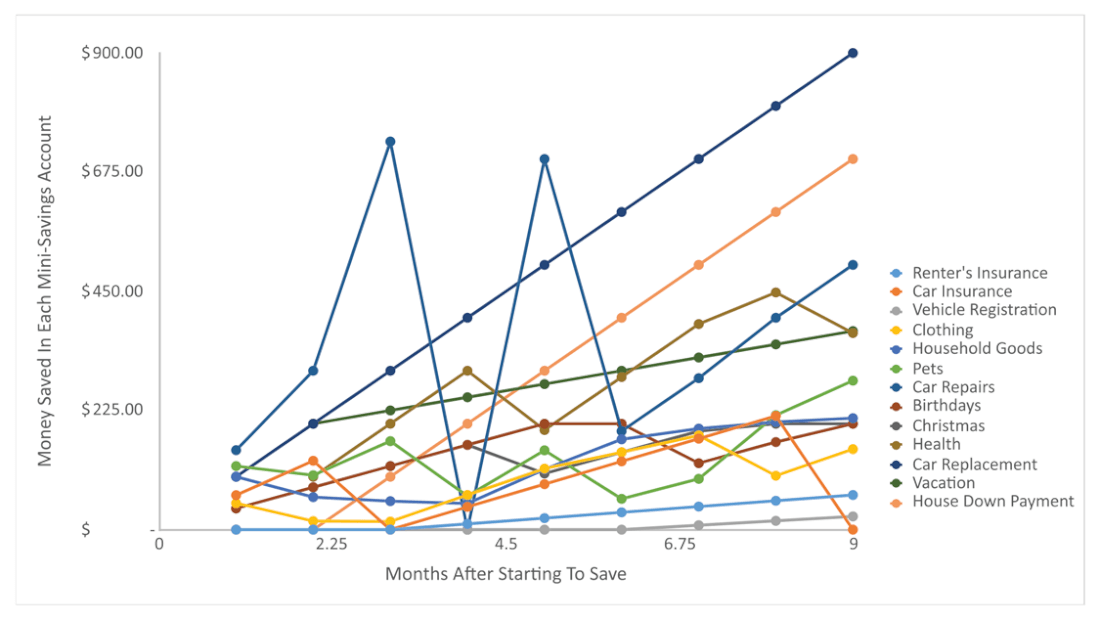

Even though all of my mini savings accounts are earmarked for certain expenses, I’ve got more money in the bank now than I ever had before. I’ve been able to break out of the paycheck-to-paycheck cycle, thanks in part to these accounts. I’ve gone from being in reaction mode to being proactive, and for the first time in my life, I’m actually starting to build wealth. We started saving up in each of our mini accounts back in August 2015, and you can literally see our wealth grow over time:

It’s about time I started building my wealth, anyways – I’m almost 29 years old!

Accelerate Your Savings With an Online CD Account — Apply Here >>