Congratulations! You’ve been accepted! These are words that make both student and parents happy. Think you can breathe easy now? Sorry. Before you send off your deposit check, you need to figure out the financial commitment.

Along comes the letter from the Financial Aid office with your “award.” The letters that many schools provide can be very misleading and confusing.

In addition to “unpacking” the information that may or may not be in the Financial Aid letter, you should be considering the financial cost of the entire degree.

This is especially true if you are comparing awards from different schools.

The Perfect Scholarship Could Be Waiting For You. Find Out More Here >>

Question #1

Are all costs included in the school’s cost estimate? We are talking about the costs of getting to and from school, the costs of actually “living” while at school (spending money beyond room and board), buying books and supplies, doing laundry, etc. If these costs are included, are they appropriate to you?

Do you live closer to or further from the school than the average student? Will you need to be traveling more or less than the average student?

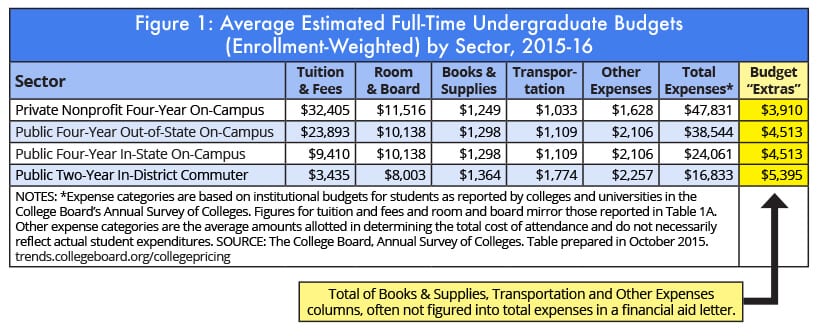

The College Board publishes average costs for college attendance that could be used as a starting point. We are talking about the three columns to the right of Room and Board, averaging between $4,000 and $5,000:

Check Your Rates for Private Student Loans — Find Out More >>

Question #2

How much will tuition go up each year? How might the financial award change each year? Is it guaranteed? If merit-based, what GPA must be maintained? If need-based, what will make it go up or down in coming years?

Question #3

How likely is it that the student will graduate in four years? It is worth asking, if it is not advertised, what efforts the school makes to help students “finish in four.”

The website collegeresults.org is a great resource for statistics on retention and graduation rates, as well as cost information, links to “Net Price Calculator” for each college, and comparable schools. It also allows you to select and compare several schools.

Once you have answered these questions, you can begin to “unpack” the letter you have received. More often than not, schools lump available loan amounts into their “aid” numbers, not differentiating between grants and scholarships, which do not have to be paid back, and loans, which do.

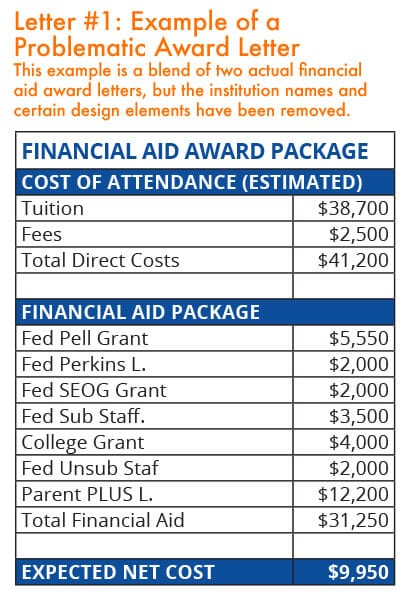

An example of a “problematic” award letter by edvisors.com is provided here.

Cut Down the Cost of College — Easily Apply to Scholarships Today >>

Note that, first of all, not all of the costs of attendance are included. Secondly, the financial aid listed is a combination of grants and various loans, including Parent Plus loans, all of which are presented using abbreviated terms. The “expected net cost” is totally misleading.

In comparison, look at the example of the “improved” award letter. It includes all costs, and correctly lists the net price before listing the borrowing options to help finance that “cost.”

Is it enough?

The final question to ask is one you ask the institution itself, preferably before you commit. You can appeal your financial aid award. It can’t hurt to ask for more.

If you have a better offer from another institution, you will have a better case. There are many online resources to help you craft this letter. The Art of Applying is just one site that offers advice.

I urge all students and their parents to thoroughly research the various loans, interest rates, and conditions of repayment before signing anything. Money is handed over to 18-year olds who rarely understand what they are committing to. Often, the parents have no clue either. Learn all about it together!