CentSai prides itself on writing independent reviews. Check out our rubric to see the objective standards we use.

Highest Possible Total Score:

After purchasing TradeKing in 2016, Ally Financial renamed and rebranded the low-cost investment tool, and Ally Invest was born.

The word ally holds many meanings outside of its dictionary definition, and Ally seems to have paid attention to the weight of this word while rebranding. The company prides itself on helping the greater good by providing economic mobility for all. Ally values diversity and inclusion through its hiring process, employee benefits, grants, and sponsorships.

Many Gen Zers choose socially responsible companies. They are also notorious for bringing attention to inauthentic expressions of social reform, especially if they are presumably exploitative. This review will not turn a blind eye to Ally’s progressive claims.

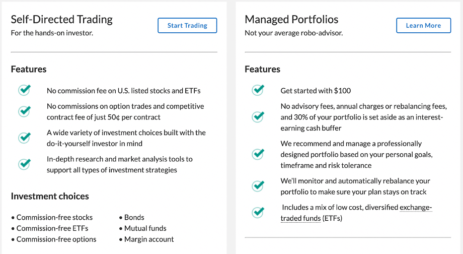

Although Ally does not provide any in-person banking services, which may be a novel idea to some, the company’s automated online investment platform is suited for a myriad of investing personalities. Say you’re more of a passive investor: Ally Invest has managed portfolio options that take the hassle away. If you prefer to be more involved, you can take the self-directed trading path.

Because the company started as an online bank, the natural progression was to make its new investment option highly integrated with its own accounts. The seamless combination makes investing through Ally especially convenient for existing Ally customers.

Here are a few factors that make Ally Invest stand out, and some pluses and minuses to consider.

Ease of Use Score:2.5

Ease of Use Score:2.5

Setting up an Ally Invest account is speedy and simple if you already have a bank account with Ally Financial. Otherwise you must go through additional set-up steps to start investing.

In general, the Ally Invest website has a standard layout and interface, which leads to manageable navigation. The site’s InvestLIVE component can be customized with different color coding and feed layout options, so you can personalize your investment interests.

The company offers managed portfolios, self-directed trading, and IRAs through both its website and mobile app.

Once you choose which account type is right for you, the account setup process begins. Ally asks questions regarding your financial status and to provide confidential documentation, such as your Social Security number and a photo of your driver’s license. This information helps Ally verify your account so that you can begin safely investing.

If you already have an Ally bank account, you can skip this process and begin investing. The integration of Ally Banking and Ally Investing allows for customers to access all their Ally Financial accounts in a singular dashboard.

Though you can trade equities and mutual funds on both the desktop and mobile versions, Ally informed CentSai that the mobile app doesn’t allow you to make fixed income trades, which is only a minor drawback for some. That being said, mobile and online transactions are fast — and updated stock quotes are available.

Bang for Your Buck Score:3

Bang for Your Buck Score:3

The true value lies in the combination of Ally Bank and Ally Invest. But if you are not looking for both, Ally Invest can still offer a variety of investment options at low rates. Let me explain with a rundown of the costs:

- No account minimum for “cash-enhanced portfolios” (defined below) and no trading commissions

- Commission-free trades on U.S. stocks, options, and exchange-traded funds (ETFs) recommended by Ally Invest

- No transaction fee for mutual funds

It’s important to note, however, that the no-fee rate applies only to Ally’s “cash-enhanced portfolios,” which keep 30 percent of your assets in cash, so you’re investing only 70 percent of your money.

Additionally, the company requires a $100 minimum to start investing with a managed portfolio. This compares to Stash Invest’s $5 minimum, and Betterment’s $0 minimum requirement.

To be able to invest 98 percent of your funds, you must open a “market-focused portfolio,” which charges a 0.3 percent fee on your total assets annually. This fee is a bit higher than one of Ally’s competitors, Betterment, as it charges 0.25 percent. The other 2 percent of your money acts as a cushion, which I address further in the next section.

Lastly, although many of its competitors offer a variety of features like tax-loss harvesting, interest-bearing accounts, and debit cards, Ally Invest grants these capabilities only to those who also have an Ally Bank account.

So, what do you get out of Ally Invest’s services? Flexibility through personalization, a relatively wide range of investment options, a highly integrated banking and investment platform, and coverage from the Securities Investor Protection Corporation, of up to $500,000 in customer claims.

Customer Service Score:2.5

Customer Service Score:2.5

Reading about the 30 percent cash hold sparked curiosity for me, but I struggled to find clear answers to my questions on the matter. What is the point of setting aside such a large portion of cash? What does the customer get out of this? Does that cash receive interest, or does it just sit there?

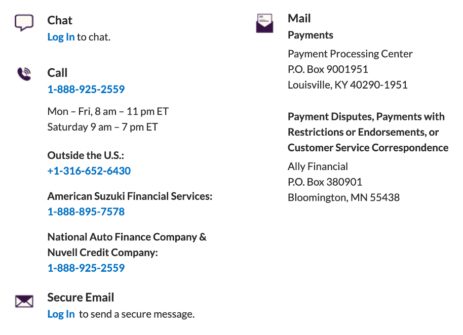

I dialed Ally’s customer service number, patiently waited on the line for about four minutes, and was then greeted by a friendly representative. They informed me that the 30 percent hold is to ensure that if the market becomes volatile, there lies a cash buffer to save you from losing it all.

The customer service rep explained that the goal is to open the opportunity for beginners to comfortably start investing with no fees.

For me, however, this brings up additional concerns. It emphasizes the risks of investing. As a customer, I want reassurance that I can put my money in the hands of this company without worrying about the need for a cushion.

I contacted Ally Invest’s press office and found that the 30 percent in cash “in a cash-enhanced portfolio acts as a cushion and earns interest at a competitive rate.” But customers have the choice of selecting between this cash-enhanced portfolio or a market-focused managed portfolio, which does not require this withheld cash.

Although my initial customer service interaction raised a personal concern of mine, the overall experience was pleasant, efficient, and I eventually got the answers I needed to feel more comfortable investing with Ally.

Reputation

Reputation

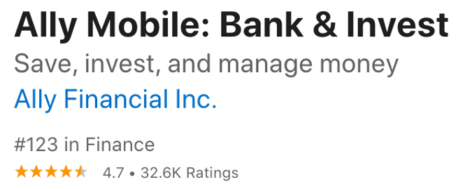

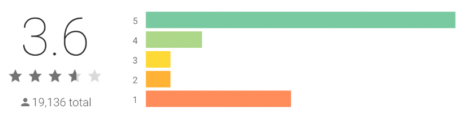

Ally Invest has a wide range of reviews and an inconsistent reputation across the board. The company exceeds expectations on the App Store, as it scores 4.7 out of 5 stars and spot number 123 on the Finance App charts.

It’s important to note that, once again, customers who are satisfied with Ally seem to be so because of the banking and investing double whammy.

But looking at Ally Invest’s Google Play reviews, the company appears to have many dissatisfied customers. Google Play reviewers express issues with the app being outdated, slow, and feeling unimpressed overall.

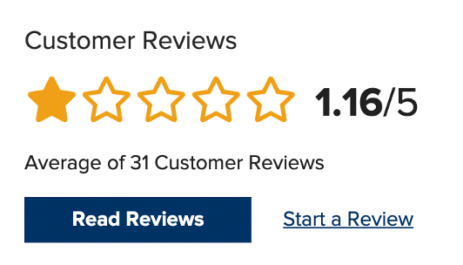

And elsewhere, the numbers don’t fare much better. The Better Business Bureau (BBB) has received 31 customer complaints, giving Ally Invest 1 out of 5 stars on the average customer review, and a D- from the website. Many of the complaints revolve around customer service, unexpected fees, and technical glitches including entire user accounts no longer appearing on its app.

In response to these negative reviews, Ally respectfully disagrees. The Ally Invest team told me that “Multiple third-party sites have given Ally Invest positive reviews. Additionally, Ally Invest is actively working to address the issues that have been raised, including focused work on customer care and platform resiliency. Our BBB complaints are handled through our sensitive complaint process and a dedicated team (Executive Complaint Resolution) escalates and handles these complaints to resolution with the client, and then notifies the BBB.”

While you’re assessing which company you should trust to invest your money, it’s startling to see these reviews. Customers commonly use review platforms to inform themselves and make high-involvement buying decisions. It appears that Ally Invest does not take these reviews lightly and that it continuously works to improve the product and the customer experience.

The Bottom Line

Ally Invest offers a tightly integrated investment system for those who also have an Ally Bank account and a plethora of investment account types that accommodate all investor types and styles. The profiles and interfaces allow for personalization for the user’s specific needs at a one-stop shop.

However, Ally Invest lacks in a few categories. First and foremost, it has a poor reputation across the web, although the company says otherwise, and we must consider Ally’s efforts that go unnoticed behind the scenes.

Though the company’s efforts of being a good “ally” are expressed, I believe there are several competing investment platforms that I may pick first.

As someone who believes in the power of allyship and appreciates companies who highlight their social values, I was moved by Ally’s words but didn’t feel the product was the right fit for me. Nevertheless, I applaud Ally for its efforts and recognize their continued attempts to improve the product and provide for their customers.

The real benefits seem to appear through the integration of Ally banking and investing. So, if you have a sister account with Ally, give the company’s investment platform a shot. If not, I would compare the online investment options out there, because it’s imperative to choose the right company to form an allyship with.

Past performance is not a predictor of future results. Individual investment results may vary. All investing involves risk of loss.