Q: Given how auto insurance works, what can be done to make it sexy?

A: Nothing.

Q: What can be done to make auto insurance fun?

A: You’re kidding, we hope…

I have a strong “dislike/like” relationship with auto insurance. For a few years, I worked for an auto insurance company. I liked that they gave me work and money. I disliked how insurance sausage was made. I didn’t like how a few people paid thousands of dollars per year for auto insurance.

A former boss said the company aimed to capture the best of the worst drivers, in more colorful language. I don’t like that I am charged more than $200 per month for cars that mostly sit in my garage. I have restarted the search for auto insurance. When people say they like shopping, they certainly didn’t mean shopping for auto insurance.

At a high level, we’re going to cover the basic terms of auto insurance in this piece. Next time, I’ll go over things that can lower your premiums as well as how to shop for auto insurance. Let’s get started.

Personal Auto vs. Commercial Auto

When most people think of auto insurance they say I need insurance for the vehicles I drive to work and for leisure. This is the personal auto market. It’s dominated by catchy TV slogans, like “Like a good neighbor, State Farm is there” or “You’re in good hands, with Allstate.” It’s dominated by well-known companies like State Farm, Allstate, Progressive, and GEICO.

There is another market, not as well known, called commercial auto, which covers plumbers, electricians, contractors, commercial drivers, and fleet operators.

You’ll be surprised to find out, if you drive for Uber or Lyft, you may need to get a separate commercial auto policy for your efforts.

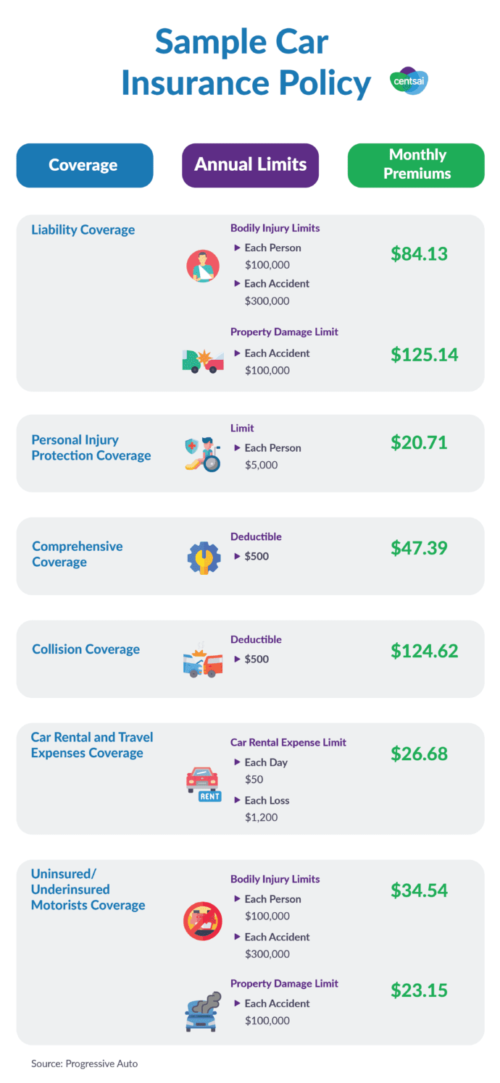

Liability vs. Physical Damage

Insurance is known for using jargon and acronyms. I will do my best to avoid it. When you buy a personal auto policy, the policy will be broken up into liability and physical damage portions. Each section will have a dollar amount associated with it for the cost.

Liability is the harm you may cause to another person or property while driving, or the harm that results when they damage you.

For example, you go through a stop sign and hit another car. The person’s injuries will be covered under the bodily injury portion of your policy. The damage to their car will be covered under property damage.

One major coverage people don’t know about is uninsured/underinsured motorists coverage.

This part protects you, if someone doesn’t have any insurance or they don’t have enough insurance to pay the damages. Your own insurance company will kick in what the other party could not pay. This is divided further into bodily injury and property damage coverages.

Physical damage covers you in two scenarios. The first is called comprehensive. Comprehensive covers you against “Acts of God” (tornadoes, earthquakes, flooding, violent winds), damage from animals, fire, theft, and vandalism.

Physical damage covers you in two scenarios. The first is called comprehensive. Comprehensive covers you against “Acts of God” (tornadoes, earthquakes, flooding, violent winds), damage from animals, fire, theft, and vandalism.

The second is called collision, and as it says, this covers your vehicle for damages if you hit something else or something hits you, regardless of who is at fault.

Unlimited Mileage vs. Pay-Per-Mile

Traditional auto insurance doesn’t charge you for each mile you drive per day. They may categorize you, based on how much you drive per year, and how far your work is from your home.

If you drive or don’t drive, the auto insurance companies don’t care. They’ll charge you the same amount every month.

New kinds of auto insurance work by charging a base amount, and then charging you for the miles you actually drive. This is called pay-per-mile. I know Root, Metromile, and Milewise by Allstate offer some form of pay-per-mile auto insurance.

The pay-per-mile auto insurance may reduce your costs if you drive fewer miles. This is one of the options I am currently investigating for myself.

Policy Limits

For each type of coverage, there may be policy limits. Policy limits tell you how much the insurance company will cover for each occurrence, and how much they’ll cover in total.

Let’s say there is an accident, and three different people are injured. The insurance policy may say, we’ll cover you for $100,000 in claims for each person, and $300,000 in total for the entire accident. These are more common with liability coverages.

Higher policy limits (increasing how much an insurance company will pay) will cost you more.

Deductibles

The scourge of normal people everywhere, deductibles ask you to have some skin in the game. There’s nothing wrong with deductibles. They do make it more difficult to figure out how much you’ll get reimbursed. This is the amount you have to cover for property damage losses before the insurance company covers its part.

Common deductible amounts are $250, $500, and $1,000.

The lower your deductibles, the more you will pay for insurance.

The opposite is true, too. If you’re willing to accept the risk, higher deductibles will lead to lower premiums. All insurance is about reducing risk, and if you have less risk, the insurance companies will charge you more for taking on a larger share of the risk pie.

Payment Plans

This is a big gotcha. If you pay for your policies monthly, you’ll probably pay more than if you paid all at once. Many places call this a paid-in-full discount. If you had an auto insurance policy for six months, and paid all at once, it might be $600. If you paid for it every month, the cost might be $105 a month, or a total of $630.

This is an easy money maker for the insurance company. Pay for the shortest time frame your finances will allow.

Length of Policy

Most auto insurance policies are six months long. There are a few that are 12 months. That means you are covered by the insurance company for a six-month or 12-month term. Insurance companies like six months, since it gives them more chances to raise your premiums if you make a claim during that time.

Auto Insurance and Auto Manufacturing Combine

Tesla’s new trend offers auto insurance for Tesla vehicles only. This is a powerful model to enforce a positive feedback loop. Tesla's auto insurance model works like this: If Tesla gets claims, they can analyze which parts of the car are more costly to repair, more likely to get damaged, and re-work their factories and vehicles to simplify repair.

Since they are well aware of the risk of their own vehicles, they can sell the insurance for close to break-even, which reduces prices for consumers. As they use this feedback loop, the cost of insurance should decline over time.

There is added convenience of having insurance accessible, easy to buy, and ready to go at purchase.

If the rise of Amazon and online shopping tells us anything, worldwide many consumers will happily pay more for greater convenience. Tesla Insurance is rolling out in a few parts of the United States.

Not to be outdone, Porsche is following Tesla’s footsteps with Porsche Auto Insurance, only for Porsche drivers. This model is a pay-per-mile program. I expect further auto manufacturing companies to launch their own insurance programs. Could this be the vaunted Golden Age of the Actuary?

The Bottom Line

Auto insurance is complicated. Much like a car, it has many moving parts. Each influences another aspect, which makes it hard for the casual shopper to understand. Next time you look at your policy, our hope here at CentSai is you have a better understanding of what your insurance policy looks like, allowing you to make better decisions with what coverage you get for your money.

Neither CentSai nor the columnist have financial ties to any products or services mentioned here within.