In this column, we’re going to explore what health insurance is, and some of the basics of your policy. Compared to any other insurance, this might be the most expensive insurance you’ll buy in your life.

Let’s get started. We’ll be using healthcare.gov’s glossary to guide us — which is a fab resource for any health insurance-related question. I have added the glossary definitions to questions and linked to the definition. Bonus: I’ll use a real-life health insurance policy from healthcare.gov to highlight practical information.

What is Health Insurance?

Health insurance is a contract that requires your health insurer to pay some or all of your health-care costs in exchange for a premium. (I’ll tell you what a premium is in a second.)

What is a Group Health Plan?

In general, a group health plan is offered by an employer or employee organization to provide health coverage to its employees and their families.

Group health plans benefit from economies of scale. The more people covered, the lower the cost.

How Many People Live Without Health Insurance?

About 33 million Americans don’t have health insurance, according to the Centers for Disease Control and Prevention. The percentage of the population that is uninsured has declined from about 15 percent in 2008 to about 9 percent in 2018.

Views may vary as to why more people are covered, but I believe the difference is due to the passing of the Affordable Care Act in 2010.

What is a Premium?

A premium is the amount you pay for your health insurance every month.

In addition to your premium, you usually have to pay other costs for your health care, including a deductible, copayments, and coinsurance.

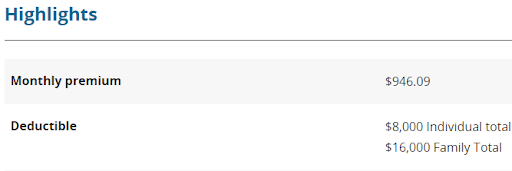

The example above is from a healthcare.gov policy for a family of two adults and two children. The annual cost of this health insurance’s premiums is $11,353.08.

What is a Deductible?

A deductible is the amount you pay out of pocket for covered health-care services before your insurance plan starts to pay.

With a $2,000 deductible, for example, you pay the first $2,000 of covered services yourself before your insurance will chip in.

In the example above, each person pays an $8,000 deductible. The family total deductible limit is $16,000. This means the entire family is on the hook for $16,000 in medical payments plus premiums before the insurance company steps in. Ouch!

What Differentiates Copay and Coinsurance?

It’s easy to get the terms coinsurance and copayment confused. Your coinsurance is the percentage of costs of a covered health-care service you pay. In this sample policy, if you go to a primary care doctor, you would pay 50 percent of the visit after you’ve paid your deductible.

It’s easy to get the terms coinsurance and copayment confused. Your coinsurance is the percentage of costs of a covered health-care service you pay. In this sample policy, if you go to a primary care doctor, you would pay 50 percent of the visit after you’ve paid your deductible.

Let’s say your health insurance plan’s allowed amount for an office visit is $100 and your coinsurance is 20 percent.

- If you’ve paid your deductible: You pay 20 percent of $100, or $20. The insurance company would pay the rest, unless the insurer restricts the maximum they will pay for a service.

- If you haven’t met your deductible: You pay the full allowed amount, $100.

A copayment, on the other hand, is a fixed amount ($50, for example) you pay for each visit for a covered health-care service after you’ve paid your deductible.

Let’s say your health insurance plan’s allowable cost for a doctor’s office visit is $100. Your copayment for a doctor visit is $20.

- If you’ve paid your deductible: You pay $20, usually at the time of the visit.

- If you haven’t met your deductible: You pay $100, the full allowable amount for the visit.

I would recommend opting for a plan that gives you more flexibility with copayments if you can, as coinsurance can give you sticker shock. In exchange for fixed copayments, you’ll pay a higher premium. If you opt for higher coinsurance, you take more of the risk, but you will likely lower your premiums.

What is an Out-of-Pocket Maximum?

The out-of-pocket maximum is the most you will have to pay for covered services in a plan that year.

Once you spend this amount on deductibles, copayments, and coinsurance for in-network care and services, your health plan pays 100 percent of the costs of covered benefits. Keep in mind: On the first $16,000 in a year for family medical bills, you pay 100 percent.

The only way to know what is covered is to do a deep dive into the policy by reading the contract.

Even if you can understand the words, it’s hard to make sense of what they mean.

Forget about reading multiple contracts. Your best bet is to ask someone in your company’s Human Resources department to summarize the policy for you.

If you are an independent small business owner, be prepared to take valuable time to understand coverage — even if you have a good agent.

Check back next week for part two as we dive deeper into understanding health insurance.