Eric Strausman

Managing money at any age is tough. Modern life can make it even tougher. We have access to more products, services, fun stuff, and distractions than ever before. But we also have more ways of staying on top of our finances than ever before. This list details some of the best financial apps that you should try — whether you’re a millennial, Gen Xer, or boomer — to find the one that is right for you.

Manage Your Money Better With a High Interest Checking Account — Sign Up Today >>

The Benefits of Good Financial Apps

Unless you have a brilliant mind (and haven’t we all, precious), it’s difficult to stay on top of the ever-mounting bills that pile up each month. And we’ve all struggled with creating a budget we can actually stick to.

These apps aim to promote financial well-being in the best way: by working closely with you and your money to lead you toward healthier finances.

If you come away from this article and don’t download at least one app, you’re either a mathematical wizard, financially stable, or crazy (no offense). So without further ado, it’s time to check out eight of the best financial apps out there!

1. Albert

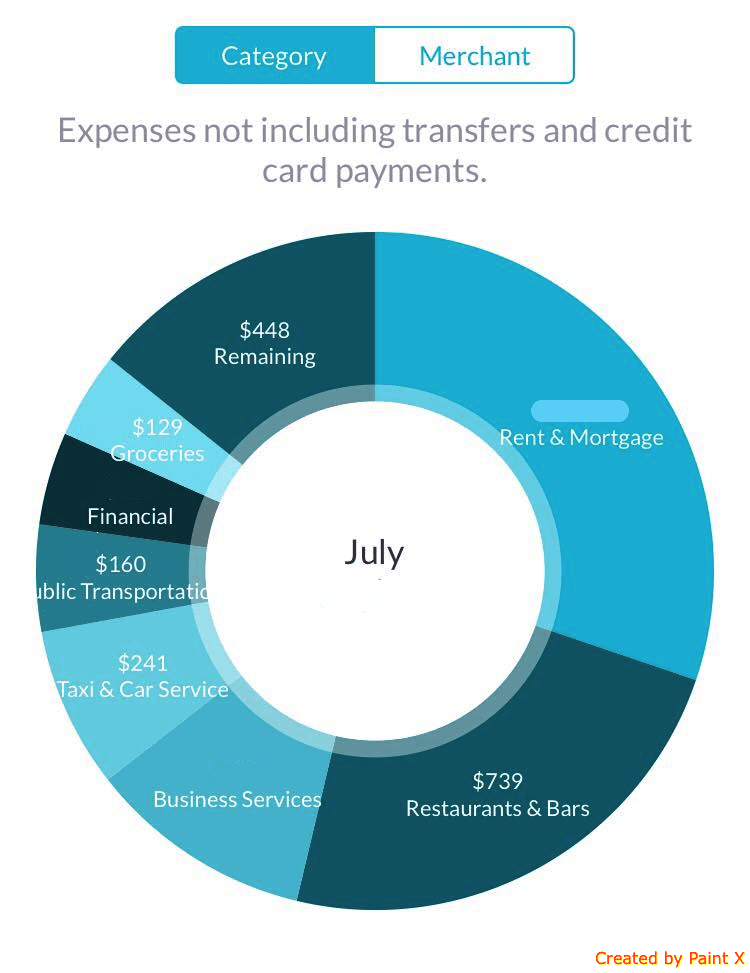

I never thought I’d fall for someone — or something — named Albert. In a twisted way, I love how he makes me feel mad guilty for the crap I spend my money on by breaking it down into a beautiful monthly infographic. (Check out the chart on the right.)

Before you start judging me, just know that I, too, was thoroughly horrified when I saw it.

But that’s the tough love that Albert provides by showing me I spent almost $1,000 on restaurants, bars, and cabs. Yes, I am in my early 20s, but still, Albert tells the truth judgment-free.

Albert is easy to set up, and once you link your bank account, he’ll analyze your income and expenditure, and advise you on the best budget to suit your needs.

He also offers the option to create a savings fund within the app. You can set the amount, and at regular intervals, it will come straight from your account and into Albert. When you need the money, it only takes two to three business days to return to your bank account. No fees!

Save Simply and With Ease Toward Your Financial Goals >>

On top of day-to-day expenses and budgeting, which are all free to access, Albert offers the “Albert Genius” option. This is a team of human financial experts available on demand.

You contact them via text message on your phone. Then they go through your expenses and can tell you where you’re going wrong and how to make it right.

You decide what you pay for this service each month, though the minimum is $4. I’m currently on the one-month free trial and received my first personalized feedback from my human Albert adviser when I asked how I could save more.

You decide what you pay for this service each month, though the minimum is $4. I’m currently on the one-month free trial and received my first personalized feedback from my human Albert adviser when I asked how I could save more.

Not only does Albert help you save, but he’s so smart that he also keeps track of your loans, investments, and credit cards bills, too.

If you don’t have any investments, Albert gives you the option of opening up various retirement accounts, private investment accounts, 529 college savings plans, and more.

Albert can also help you compare different insurance policies in order to save money. If I was an American citizen, this app would be able to help me control every aspect of my financial life. Albert has stolen my heart. Sigh.

2. Mint

I’ve been using Mint for a while, and I was a huge fan at the start. But other apps have overtaken it in terms of accuracy, ease of use, and general helpfulness.

The app is designed to keep all your bills in one place so that you're aware when they are due. It does this okay, but doesn’t link very well to the actual account from which you pay those bills, and thus can be a little behind the times. As in, it might show that you have money to pay a bill that you actually don’t, and wouldn’t that be heartbreaking?

Save Without Ever Lifting a Finger — Learn More >>

Mint also tracks your spending, but it has an odd way of categorizing it. This month, it told me I spent $35 on gas and fuel, but I don’t own a car. Hmmmmm.

It also sets weird budgets on my spending that I seem to have no control over. For example, it tells me I’m allowed to spend only $50 a month on dining. Girl, I can spend this in one day. Don’t test me.

It’s not great at keeping your bank balance updated, either. In fact, it’s usually off by a couple of days. This brings me false hope on those days before payday when it tells me I still have $200, but in reality, it’s more like $50.

It’s surprising that it could be so slow, given that it’s run by Intuit, which is a big dog in the finance world.

One thing I do like is that it tells me when I’ve spent more than usual on a particular item or activity. For example, “Kelly, this week you spent $1,293 on personalized teapots when you normally only spend $856.”

It’s messages like this that help keep me on track. Okay, yeah, I'm joking about the teapots. But you catch my drift.

3. Wally

Voila, another app for tracking your expenses, credit cards, loans, and even shared accounts. I’ve not yet managed to convince a man to share an account with me, so that last part is sadly useless at the moment. Come to think of it, do I want some gold digger having access to my hard-earned funds? I think the frick not!

For some reason, it offers two apps, Wally Lite and Wally Next. When I downloaded the former, I was encouraged to actually download the latter. Financial apps are strange.

I decided to stick with the recommended Wally Next, maybe because the “n” made me feel clever. Setup is straightforward and done within the app. The cool thing is that Wally lets you add foreign accounts to track, too. Even though my Irish account is completely empty, it’s nice to know someone cares.

It does not, however, let you link to your bank account directly — you have to keep it updated yourself. I'm lazy, and I know I won’t have the time nor the inclination to remember my balance when apps like Albert will do it for me.

No Credit Check Needed — Apply for Your Secured Credit Card Here >>

Admittedly, apps that have direct access to my account and can see for themselves what I’m doing are scary when I put it in those terms. But they make my life so much easier, so I’m willing to ignore the Big Brother factor.

Sorry, Wally — you’re too polite for me.

4. Prism

Similar to Mint and Qapital, Prism collects all your bills in one place, and helps you to pay them through the app.

Honestly, I’m not too fond of Prism, and I’m beginning to think that maybe I just don’t want to see all my bills in one place. It requires a lot of initial setup without much introduction as to what the app can actually do for you.

While it is handy that you can pay all your bills simultaneously, the setup is heavy. Plus, if you don't give the app all your information immediately, its functionality is low.

Happily, it doesn’t charge you anything to pay all of your bills through the app. Plus, there's even the option to schedule the payments in advance. That way, you’re always on top of things.

This doesn’t work for me, as I don’t have many bills that don’t get taken straight from my bank account periodically anyway. But if you have so many that you’re failing to keep track, this app might be for you.

5. Wealthfront

Wealthfront is an investment service that takes control of your finances. Once you link up all of your most important accounts, it analyzes your finances to decide what kind of financial ninja you are.

It assesses the type of investor you are and tailors its services to suit your preferences.

Wealthfront’s approach to investing seems a little more austere than others. I’m intimidated by its wealth of knowledge on investing, and how it wants to take over every aspect of my finances.

Its website uses jargon that I don't understand. However, while making me feel stupid, paradoxically, this stuff also makes me trust the app in an odd, parentlike way.

The setup process is long. It asks for your email so you can see your personalized plan. Then you have to set up an account through a web browser, not the app itself, which is odd.

It charges a 0.25 percent annual advisory fee. So unless you plan on making tens of millions, it’s not a lot of money to spend in comparison to many other financial apps.

The minimum initial deposit in your investment portfolio is $500. Sadly, I do not have that kind of money to spare right now (nor do many of my friends.) However, I’m glad that my visa status doesn’t seem to be a turn-off the way it has been in the past.

Maybe in the future when I am inundated with money, I’ll stop by Wealthfront again and let it take me under its big, scarily knowledgeable wing. Watch this space!

6. Blooom

If you’ve already got a 401(k) retirement savings plan up and running, this site will help you manage it in an unbiased, financially sensible way. If you don’t quite understand what your 401(k) is, does, or could do, Blooom’s got you covered.

The founders of Blooom were fed up with financial services being tailored to only the top one percent. Financial advisers often don’t help those with lower incomes.

Blooom offers a free version that gives you a quick analysis of your 401(k) and how you could improve it. Then there's the paid version. The $10-a-month account gives you monitoring and management services that are customized to your particular situation, helping you to grow (or Blooom) your 401(k).

Manage Your 401(k) Today — Start by Getting Your Free Analysis >>

7. PocketSmith

PocketSmith is a highly customizable financial app that puts you in the driver's seat with a clear and continuous view of your past, present, and future finances. This money-management app securely connects to multiple banks all over the world to help track accounts in multiple currencies.

Within PocketSmith, you can track, budget, and gain better clarity across your finances with the app's tools. These include income and expenses, cash flow, and net worth statements.

The app allows you to set up a personalized spending trend based on the above. You can then forecast your finances by these trends to predict future outcomes based on your current budgeted spend.

PocketSmith currently offers three subscription levels. The basic plan is free and tracks two accounts, as well as manual transaction importing with a six-month forecast. The premium plan tracks up to 10 accounts with automatic bank feeds and provides a 10-year forecast. And the super plan tracks an unlimited number of accounts with automatic bank feeds and offers a 30-year forecast.

The Final Countdown: The Best Financial Apps in My Book

Will I continue to use all of these personal finance apps? Definitely not. I’m a huge fan of Albert, as he holds me accountable in the most visual way. I’ve used Mint for a while now, but I no longer like the way it works, so I’ll probably delete it after this article is done.

When I get a 401(k) and a couple of thousand dollars to spare, I’ll make sure to check out Blooom and Wealthfront again in order to maximize my future wealth. But until then, they'll remain firmly on the app store shelf.

Get Food, Drinks, and Groceries — Anytime, Anywhere >>

I do think that having a personal finance app that holds you accountable for good money habits and helps you stay on top of bills is a necessity nowadays. It’s far too easy to overspend with little to no regard for better uses of that money.

Take Albert. After showing me I have an “eating out and cab spending” problem, I’ve been virtuous so far this month, eating out only once. That’s the sort of behavioral change that a good financial app can encourage. I am not perfect, nor does the app ask me to be. It just wants me to think before I spend. A big ask for someone like me, but I’m getting there.