Investing is difficult for many reasons. I’ve heard countless people say they can’t find the money to spare after they have covered their monthly expenses. Sure, everyone has their own sets of budgetary constraints. Whether you’re just getting on your feet after leaving home, after getting married, or after having a child, finding money to invest is always a challenge.

As of April 2018, 59 percent of Americans report that they enjoy saving over spending, and 26 percent say that spending less overall is something they plan to continue as they move forward in life, according to a survey conducted by Gallup, the global analytics company.

So this might explain how more Americans are saving more even though wage growth isn’t keeping up with the rising cost of living. There are many different ways you can begin saving with future investments in mind. If you’ve already reviewed your budget and cut corners where you can, consider the following:

This App Makes Managing Your Finances Easy — Start Budgeting Today >>

1. Your Employer’s Retirement Account

If you are a full-time employee, contributing to your employer’s retirement plan is often one of the easiest ways to invest money without feeling the pinch. You can set up automatic deductions from your paycheck that are withdrawn before taxes are taken out.

Automating the process one of the most foolproof ways to make sure that you invest some money from every paycheck.

What’s even better is that many employers match your contributions up to a certain point. This means that every dollar of your own money that you invest turns into more than one dollar instantly. Some employers match dollar-for-dollar up to a certain percentage of your salary, while others contribute only 25 cents or 50 cents per dollar.

What’s even better is that many employers match your contributions up to a certain point. This means that every dollar of your own money that you invest turns into more than one dollar instantly. Some employers match dollar-for-dollar up to a certain percentage of your salary, while others contribute only 25 cents or 50 cents per dollar.

Either way, it’s free money that you can’t pass up if you’re looking to find more to invest. My wife and I always invest in our employer retirement accounts at least as much as is needed to get the full retirement match.

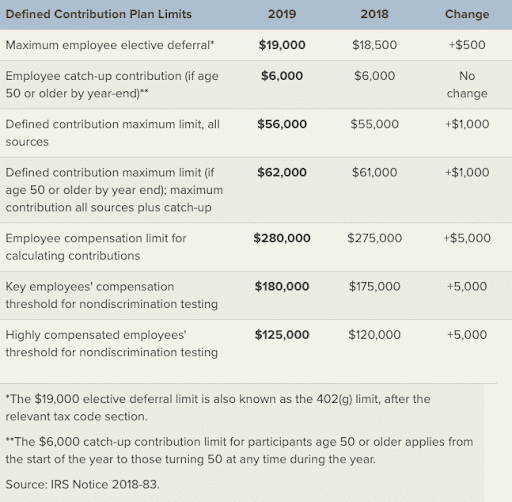

Even if you're lucky enough to have tons of room to save, you can’t contribute more than $19,000 of your own money to your 401(k) in 2019. However, if you're over 50, you’re allowed an extra $6,000 a year as a “catch-up” contribution for a total of $24,500 annually. Make your earnings work for you.

See How Your 401(k) Stacks up in Minutes — Start by Getting Your Free Analysis >>

2. Automatic Contribution Increases

Another awesome feature that many employer-sponsored retirement plans have these days is automatic increases in contributions. All you have to do is select an amount, and your employer will automatically increase your contributions by that number for each requested period. Most plans offer increases in terms of percentages on an annual basis. However, some plans offer even more choices.

You really won’t miss the money because the amounts are usually so small that you won’t even realize that they’re gone from your paycheck.

If you start out investing five percent of your salary and increase that by two percent every year, you’ll eventually invest 15 percent of your salary in just five years. If my wife and I weren’t already at our ideal percentage, this is exactly how we’d start increasing the amount we invest.

3. Half of Every Raise

Investing half of your raise is a genius way to find more money to invest. In order for this trick to work, you must increase your investment amount as soon as you receive your raise. Otherwise, you might incorporate your extra raise money into your budget and avoid investing it after a paycheck or two.

You’ll still be able to access the other half of your raise for whatever you wish, though. Personally, my wife and I love this idea because it not only helps us prevent lifestyle inflation, but will also help us retire sooner. It’s a win-win situation in our eyes.

Learn How to Invest Confidently — Download This Free App >>

4. The “Pay Yourself First” Method

If you don’t have an employer-sponsored retirement account, you can still find ways to invest money. The easiest way to do so is paying yourself first. Essentially, you decide how much you want to invest. Then you go to your investment provider and set up automatic transfers that will come out of your checking account the day after your paycheck is deposited.

This way, you won’t simply invest whatever is left over at the end of the month. Instead, you’ll invest the same amount each paycheck. My wife and I use this method to fund our Roth IRAs.

You can also implement the automatic increases that some employers offer with just a bit of work. Pick your go-to calendar application and set future reminders to increase your contributions as often as you want. When the reminder goes off, increase your automatic transfer amount.

5. The Monthly Expenses That You Don’t Value

This method has the greatest upside when it comes to finding money to invest. All you need to do is take a look at your monthly spending. Make a list of your expenditures and put a mark next to categories that you feel don’t give you enough value for the money you lay out. These could be dining out, car payments, memberships, subscriptions, or any number of other expenses. Then cut back your spending in those categories and use the money you save to start investing.

The Bottom Line on Different Ways to Invest Money

Finding ways to invest money doesn’t have to be difficult. You simply have to be decisive in your mindset, knowing that you don’t have to start with a large nest egg. That is built over time with good habits and the magic of compound interest. Once you see how much it benefits you, you'll be investing on a regular basis in no time.

Even if you don't have much money, you might want to set yourself up with an automated app like Stash, where you can invest as little as $5 at a time. Build an investment strategy that suits your goals, risk levels, and budget. Plus, get updates, tips, and articles that allow you to continue to learn as you invest.

Invest in the Companies You Believe In, With Any Amount of Money — Download This Free App >>

Additional reporting by Jazmin Rosa.