Confession: I am extremely lazy when it comes to budgeting. I’ve reached a point where I try to do the least amount of work possible in tracking my expenses. Yes, I am fully aware that, among fellow mega money nerds, this may be deemed a cardinal sin. But why bother to fix something that isn’t broken?

Before there was a surge of budgeting apps, I used a spreadsheet to track my expenses. I used to obsess about budgeting apps and was eager to jump on the bandwagon to try them out.

Now, I use own system to manage my money and have put using digital tools on the back-burner.

For those who want to put in minimal effort – or who hate thinking about money altogether – here are a few pointers on how you can structure your budget to help you put things on autopilot with confidence.

Get Help With Budgeting Today — Download the Personal Finance App Here >>

Create a System

Having gone through the trial and error of figuring out what works for me, I’ve found that the easiest, most foolproof thing to do is to create a system for easy flow of money into whatever priorities you’ve set.

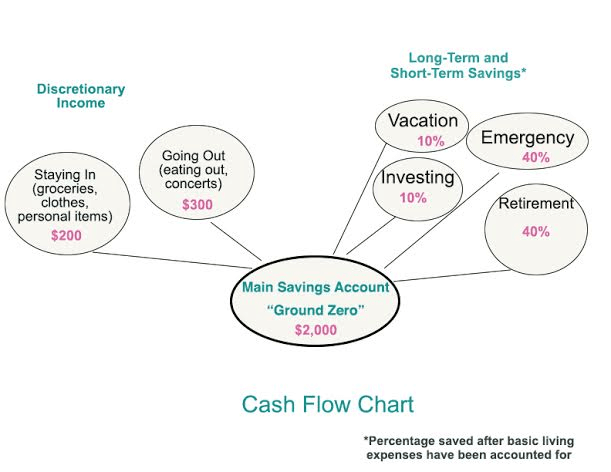

I dump my income into my main checking account. This serves as a sort of take-off point for my finances. Money that sits in my main checking account is used to pay my bills. But some is also funneled to my buffer fund for short-term emergencies, to a main emergency fund, to retirement savings, to a “fun” fund for vacations and mini-splurges – what have you.

Find the Right Checking Account for You — Apply Now >>

When it comes to my discretionary spending – or anything other than my rent and utility bills – I’m a huge fan of the “island approach.” What this means is that I isolate my money into categories so that I can best monitor them.

For instance, I have a separate debit card for my “going out” expenses – such as going out with friends and going to concerts. I have another debit card for “staying in” expenses, such as groceries and buying personal items.

I put the same amount into each “island” every month.

As long as I don’t go overboard elsewhere, I’m allowed to spend my money without having to track every single penny. Isolating my money this way makes it easy for me to see what’s going on and to make tweaks as needed.

Opening a Savings Builder Account is Easy — Get Started >>

Now, you may be scratching your head thinking, That sure sounds like a lot of work Jackie. But once you put in the effort up-front in creating a system, things will be on autopilot, which will save you tons of time down the line.

Trust me— I devote very little time to budgeting every month because of my system.

Automation is King

While automation remains a point of debate among personal finance nerds, I’m a big fan of it. I automate all my bills. Before I turned to freelance full-time, I automated my short- and long-term savings goals. Whether I was saving for a new computer, for a swift new bike, or for a weekend getaway, socking money away this way pulled me back on track, even when I deviated from my normally frugal self.

But what if you’re worried that you’ll be billed incorrectly or a suspicious transaction might go unnoticed? Well, one thing you can do is to receive email notices for your bills and when you put more than, say… $100 on your credit card.

Pro tip: creating a separate email account for these types of notices will help keep things organized.

To App or Not to App?

Let me make this clear: I’m not against using a budgeting app. I’m just against relying on one for all your budgeting needs. While these apps give you a lot of data, the information only proves as useful as the insights we gather from it.

So filter through the noise. Only pay attention to what you’re trying to figure out. Otherwise, your head will start swimming in a confusing digital sea of transactions and bank fees.

Someone once said, “It is only by being lazy that we become truly efficient.” By laying the groundwork and creating a tailored system for tracking and spending your money, you’ll have a process in place that caters to your personal preferences and style.

Plus, you’ll feel more at ease about spending your beans without having to monitor your spending like a hawk. And that, my friend, is where you can reap the benefits of being lazy. Have fun!

Start Managing Your Finances — Download This Personal Finance App Here >>