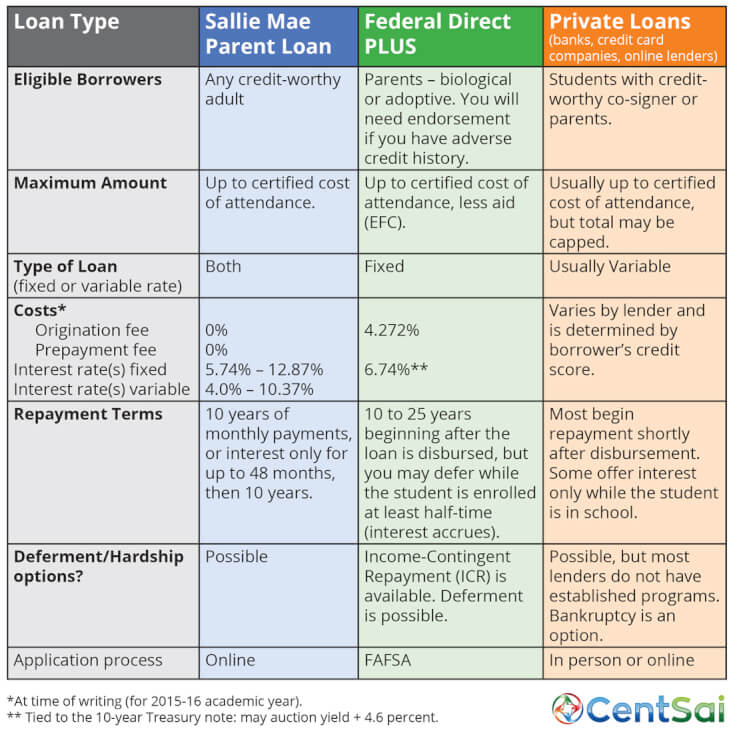

The newest entrant into the market for parent student loans has actually been a key player in the student loan market since day one: Sallie Mae. They have introduced the Sallie Mae Parent Loan.

The loans have certain features that differentiate them both from other private loans and from the Department of Education Direct PLUS loans.

Sallie Mae (Student Loan Marketing Association) was established in 1973 to service Federal student loans. It is now a publicly traded entity whose primary business is making private loans for education at all levels. It has almost $13 billion in assets, and its loan servicing operations were spun off in 2014 to form Navient, another publicly traded company.

Get Your Personalized Loan Offer in 3 Easy Steps — Find Out More Here >>

The Sallie Mae Parent Loan can be described as a hybrid of federal loans and other private loans. It has more options than either of them.

For example, any credit-worthy individual can borrow under this plan for a student’s education — an aunt or uncle or grandparent, not just a parent.

Borrowers can choose between a fixed-rate plan (like they can with federal loans) and a variable rate plan (as with almost all private loans). They also have the option of paying interest only while the student is in school (up to 48 months), and then beginning repayment over 10 years. Alternatively, the borrower can start the 10-year repayment clock with the first amounts borrowed.

One key differentiator with the Sallie Mae Parent Loan is that there is no origination fee. The Federal Direct PLUS loans currently charge a 4.272* percent fee upfront.

So what is the potential downside? Federal loans seem expensive, especially with the upfront origination fee, but if your credit score is not particularly high, this could be the cheapest option. Direct PLUS loans have fixed interest rates going in their favor, and the Federal Direct PLUS loans are the only loans that offer discharge of the debt if the school closes.

Get a Free Credit Repair Consultation — Visit Site >>

Sallie Mae Student Loan Forgiveness

They also offer the possibility of deferments for financial hardship, and while they do not offer as many income-based repayment plans as loans given directly to students do, there is an Income-Contingent Repayment (ICR) plan available that limits monthly payments to 20 percent of disposable income.

After 25 years of payments, balances on the loans are forgiven.

Another thing to keep in mind is that if a parent applies for and is denied a Direct PLUS loan, the student will be able to borrow more than the standard amount under the student direct loan programs, with better interest rates and more income-based repayment options down the road.

As with most things in the financial world, those with the best credit have the most and the cheapest options. In addition to qualifying for the lowest available interest rate of any of the private student loans, credit-worthy homeowners also have the option of tapping into their home equity to finance a child’s education.

When borrowing, it is very important to comparison shop.

While certain private loans look attractive upfront, they could be quite costly if you do not have the highest credit score, and the lender may not be flexible in the event that you run into financial difficulty.

Be sure to review the links to both the Federal Direct PLUS and Sallie Mae Parent loans as a starting point. Most financial advice articles suggest that private loans should be a last resort.

However, if you need to pursue private loans, there are several sites available to help you comparison shop. FinAid.org is an objective, unbiased source of information about all aspects of student aid and borrowing. They offer advice on what features to look for in these sites, and evaluate several of the most common ones for you.

Bottom line: This is a case where parents and students need to do their homework before school starts. It will literally pay off in the end.