Jonan Everett

What’s the best debt payoff plan? If your mind jumps to the debt snowball or the avalanche, you might be right. Or you might be wrong. People who are serious about eliminating debt can’t blindly commit to just any payoff plan. Instead, you need to build a custom plan that will keep you motivated, help you change your behavior, and protect you from financial risk. Here’s how to get out of debt with your own personal strategy:

- Assess your situation

- Evaluate yourself

- Do the math

- Figure out terms

- Realize your strengths and think about strategies

- Create your debt payoff plan

Step #1 — Assess Your Situation: Why Am I in Debt?

A decent payoff plan doesn’t start with a strategy. It starts with a question: Why are you in debt?

- Is it because a sudden illness or injury forced you out of work?

- Did you finance your failed business on credit cards?

- Maybe a high-school guidance counselor urged you to accept admission to an Ivy League even though you couldn’t afford it.

- Perhaps you’ve undergone a period of low income accompanied by a few small emergencies like car repairs.

- Some people go into debt for shoes or fancy cars or cell phones.

- Other people just don’t pay attention to their money until they don’t have any more of it.

If you know why you’re in debt, you can better figure out how to get out of it.

Do you have a knowledge problem, a spending problem, an income problem, an attention problem, a motivation problem, or a luck problem? An honest answer to this question will help you make a real plan to avoid further debt in the future.

Settle Your Debt — Get Your Free Consultation Here >>

Step #2 — Evaluate Yourself: What Could I Have Done Differently?

I constantly urge people to ask themselves, “Knowing what I now know, would I do anything differently?” Would you have skipped the fancy degree? Would you have tried to save more cash before starting your business?

Sometimes the answer is no. Some people are happy about the decisions that they made, even though they went into debt because of them. I don’t think there’s anything wrong with feeling happy about your past decisions.

The point of this exercise isn’t to kick your past self for your stupidity. The point is to help you understand that you could have made a different decision in the past, regardless of how you feel about it now.

Step #3 — Do the Math: Add Up Your Total Debt

Now that you’ve got your head on straight, it’s time to make a debt attack plan. And that starts with adding up all your debt. When you add together every cent (including overdue bills), how much do you owe — $5,000? Or maybe $500,000?

Too many people refuse to do this simple exercise. But how will you ever become debt-free if you don’t know how much you owe?

Struggling to Pay Off Your Debt? Talk to a Professional Today for a Free Consultation >>

Step #4 — Figure Out the Terms of Your Debt

Once you’re over the shock of your total debt, you need to figure out the terms of your loans to know what’s at stake. After that, you may need to make a debt snowball or avalanche plan. Or you may consider strategic default and bankruptcy protection.

I believe that all people should try to honor their debt commitments. However, I also believe that you should prioritize your family’s well-being above that of your creditors. Sometimes your debt commitments just have to wait.

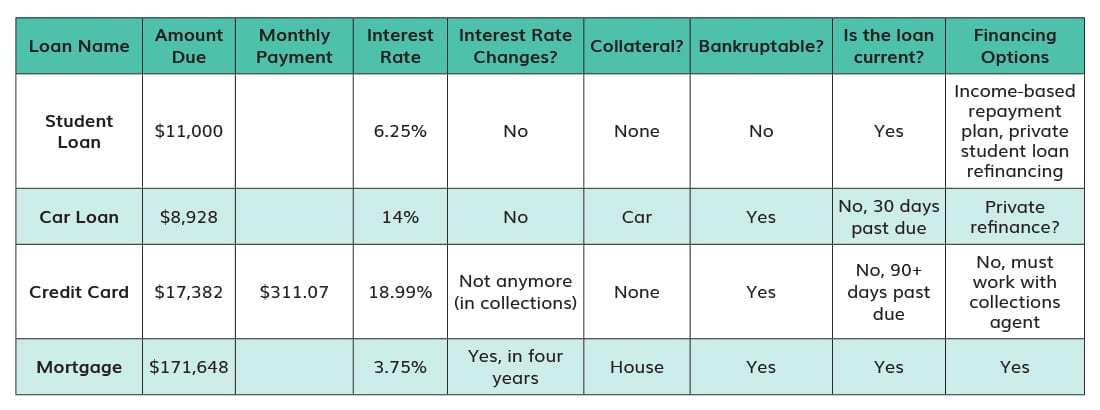

Use this table to help you understand the terms of your debt:

All these terms matter because you need to understand your risk. This is especially important if you’re struggling to meet your minimum monthly payments. Laying out the terms like this will also help you see where you have opportunities to refinance your debt and where you can make the most progress.

Step #5 — Know Your Strengths and Consider Strategies

You only need to know one more thing before you plan to eliminate your debt: You need to know yourself and your strengths so that you can take advantage of them in your payoff strategy. You may also want to take the following actions:

Big Wins

Sell everything in sight, put recent windfalls towards your debt, drain your savings account, and push reset on your life. If you’re committed to being a saver in the future, then this is a fast way to become debt-free.

Focus

Debt snowball and avalanche plans harness the power of your focus. You figuratively stare down your debt as you cut your expenses and raise your income. A lot of people struggle to maintain focus and spend years and years paying it all off. But with the exception of particularly large ones like mortgages, most people who choose one of these tactics can become debt-free in just two or three years.

Income

If failed businesses got you into debt, then successful businesses can get you out. If you’re the type of person who can earn $200,000-plus per year, then you need to focus on income, income, income. Put as much money towards your debt as you can. Don’t clip coupons — just earn more money and eliminate it.

Bankruptcy

Most people can eliminate their debt by using one or more of the strategies above. But if you can’t, you need to start thinking about bankruptcy. It may seem scary, but it won’t ruin your life. Connect with a counselor from the National Foundation for Credit Counseling to learn more about your options.

Step #6 — Make Your Plan

Your plan should include ideas for cutting your expenses and raising your income. Depending on your situation, you may want to make a list of loans to refinance or consolidate. You may even make a plan for how you’ll deal with unplanned events like emergency car repairs.

Most payoff plans also include an order of operations. Which loan will you pay off first? Which one will you payoff second? Third? Last?

Finally, use online calculators to figure out a debt-free date. Every extra dollar you throw towards payoff will bring that date closer.