We have all heard somebody (whether a friend or a TV show character) exclaim that a small amount of income has pushed him into a higher tax bracket, costing him a fortune in increased taxes. Our hearts go out to the person. Unless, of course, we know that it just doesn’t work like that. So how do tax brackets work? Well . . .

The United States has a progressive tax system. In other words, the more income you make, the more tax you pay on that higher income. But not on your prior income!

Aside from the merits of being able to explain to your coworkers why the aforementioned sad story isn’t true, there are some useful aspects of understanding tax brackets, tax rates, and how they work in our system.

Get the Most out of Your Refund — File a Free Federal Tax Return >>

How Do Tax Brackets Work?

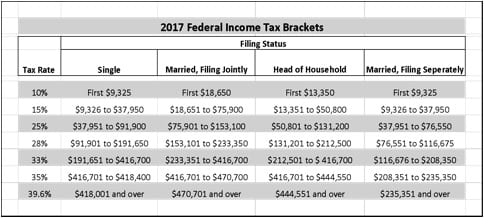

A tax bracket is a tax rate you pay on a range of taxable income. Note that this is not all of your income, only the taxable portion (as we talked about when discussing tax returns last week). Your tax brackets are dependent on your filing status. The chart below should help to clarify how this works.

For example, a taxpayer filing as single would pay tax at a 10-percent rate on the first $9,325 of her income. This equates to $932.50 in taxes ($9,325 times 0.10). If this taxpayer had $10,000 of taxable income, she would pay tax at a 10-percent rate on the first $9,325, and at a 15-percent rate on $675 ($10,000 minus $9,325).

Her total tax liability would be $1,033.75 ($9,325 times 0.10, plus $675 times 0.15). Increasing the taxable income from $9,325 to $10,000 didn’t affect the tax paid on the first $9,325. It only resulted in a higher tax rate on the additional income.

Most taxpayers fill several tax-rate buckets. They pay tax at 10 percent on one portion of their taxable income, at 15 percent on the next portion, at 25 percent on the portion after that, and so on.

What Is Your Marginal Tax Rate?

Your marginal tax bracket is the highest bracket that you’re in — or the one that you are in for the next dollar of income. Unless, of course, you have completely filled a bracket to the last dollar. In that case, the next dollar goes into the next higher tax bracket. This number can have some importance.

As such, your marginal tax rate is the rate at which you are taxed on your last dollar of income. For example, if you have a filing status of “married, filing jointly,” and your taxable income is $80,000, the rate that you paid on the last dollar of income — or your marginal tax rate — was 25 percent.

The marginal rate can also be defined as the rate at which the next dollar of income will be taxed. In general, the two definitions will produce the same result.

In other words, your last dollar taxed will be at the same rate as the next dollar would be. It’s only when you’re up against the edge of a bracket that there could be a difference. It really doesn’t matter which definition you use, as long as you understand where you are.

Your marginal tax rate is very important. It can help with making financial decisions, such as whether or not to give money to charity or whether you should make an additional pre-tax contribution to a retirement plan.

If you have a 25-percent marginal tax rate, a charitable contribution of $1,000 dollars can save you $250 in federal income tax. Likewise, an additional pre-tax contribution of $1,000 into an IRA would also save you $250.

See How Your 401k Stacks up in Minutes — Start by Getting Your Free Analysis >>

In either case, you need to know whether or not you are up against the edge of the bracket, in which case you would need to do some additional calculations.

For example, if you’re married filing jointly and have a taxable income of $76,000, the tax savings would be smaller than illustrated above because you’re only $100 into the 25-percent tax bracket. As such, the majority of your savings would be at a 15-percent tax rate.

It’s not complicated — you just need to look at the big picture.

Your marginal rate can also be important for determining the after-tax value of an opportunity.

For example, let's say that you have a chance to make an additional $2,080 per year by taking a job 10 minutes farther away from home. Forty dollars a week for 10 extra minutes a day doesn’t sound bad, right? Well, make that 20 minutes, actually — 10 minutes more to get there and 10 to get back.

At a 25-percent marginal tax rate, the $40 becomes $30 net. And you have your FICA taxes in for 7.65 percent, or $3.06. So now you're down to $26.94 for an hour and forty minutes of drive time per week. You end up with $16.16 per hour for your additional time, not considering any additional cost of driving.

Of course, there are also other factors, such as how the opportunity fits in with your career plan. But you can see how simple it is to determine what you really get from the opportunity financially speaking.

What Is Your Effective Tax Rate?

Many people consider their effective tax rate to be more important than their marginal rate. It’s definitely important, but alas, it does not have as much practical application. Your effective tax rate is the overall rate you are taxed at — your total tax applied to your total income. Let’s look at a simple example:

Suppose that we have a couple who’s married filing jointly with no children or other dependents. They’re renters and they use the standard deduction — the simplest of tax situations. Let’s say that they have a combined income of $100,000. With two personal exemptions of $4,050 and a standard deduction of $12,700, their taxable income is $79,200.

From our chart, we see that they are in the 25-percent bracket. Calculating the amounts from their three brackets, we find they will have a federal tax liability of $11,271.50 on their $79,200 of taxable income. Or, if math is not your friend, you could use the 2017 IRS tax tables and look up the answer.

That $11,277.50 of federal income tax is 11.3 percent of their $100,000 in combined income. This is their effective tax rate. Essentially, it’s your federal tax burden as a percentage of what you make. Aside from fascinating cocktail party conversation, it has little practical application.

Get the Most out of Your Refund — File a Free Federal Tax Return >>

The Bottom Line on How Tax Brackets and Tax Rates Work

If you are in the income realms in which itemized deductions or personal exemptions are phased out, you may need to do more detailed calculations. For the average person, that won’t be a factor.

Now that you’re informed about these matters, you can see how making pre-tax contributions to a retirement plan may reduce a person or couple’s tax liability, and you can calculate the amount of the reduction.

Knowing your marginal rate — and where you are in the tax-bracket schema — allows you to precisely calculate the net after-tax financial impact of a variety of scenarios. This puts you in a position to make better-informed financial decisions.

Knowledge is power. You are now more powerful. Go forth and conquer the world of personal finance.